Executive Summary

In mid-February a positive retail sales report showed a full recovery back above pre-pandemic levels and an all-time high in notional terms. Along with soaring home prices and improving industrial production numbers the goods sector serves as a stark contrast from the writhing services sector. The services sector accounts for more than 2/3rds of the GDP in the United States and its rebound is crucial for the economy to return to growth in the long term.

The most recent weekly unemployment claims was 730,000, a decrease of 111,000 from last week and part of a longer term downward trend that points to slowing layoffs across the labor market. As a reference last March saw claims higher than 6.8 million. However, the total number of people receiving some form of unemployment benefits rose by more than 700,000 to over 19 million individuals indicating the difficulty in finding new jobs for the unemployed.

While the official unemployment rate still stands at 6.3%, both the Treasury Secretary Janet Yellen and Federal Reserve Chair Jerome Powell have stated that they believe the unemployment rate is closer to 10% due to misclassifications and individuals dropping out of the labor force entirely due to childcare.

This comes at a time that Congress is preparing to pass to pass another COVID-19 relief bill that will total approximately $1.9 trillion and consist of stimulus checks, extended unemployment benefits, tax credits, funding for COVID relief programs, and aid to state and local governments. All this additional stimulus has pushed bond yields higher as concerns mount about rising inflation and the possibility of the Fed needing to reverse course and raise interest rates to stem an overheating economy. The 10-year and 30-year treasury yields have risen over 54% and 30% from the start of the year and are now yielding 1.44% and 2.17% respectively. While the levels of interest rates still sit at historically low levels it is how quickly rates have increased that is creating uncertainty and unnerving the markets.

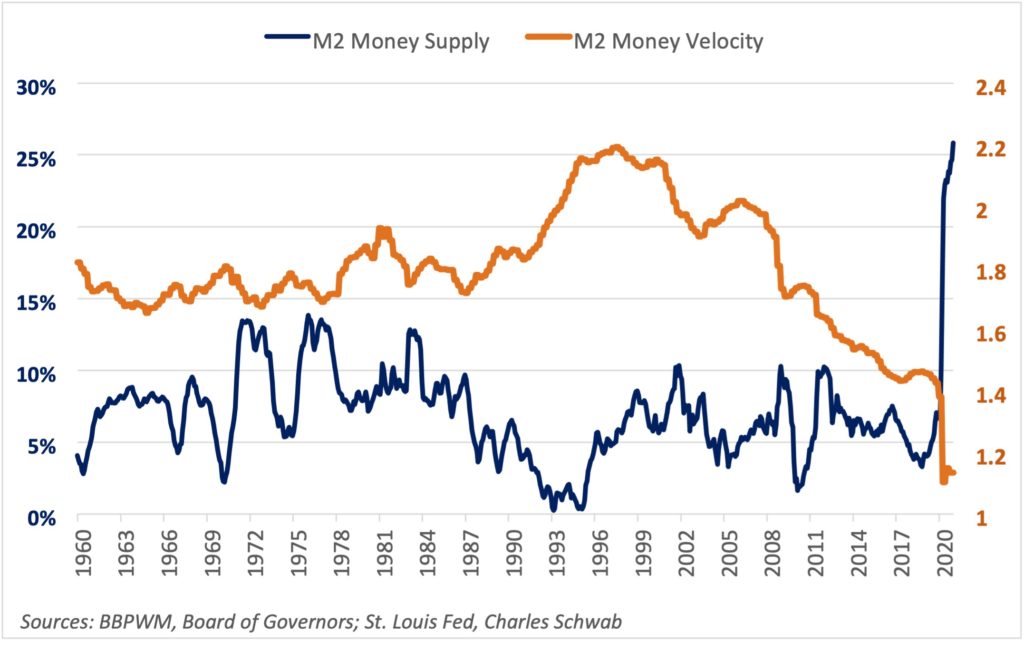

The Core Personal Consumption Expenditures (PCE) Index, which is the Fed’s preferred measure of inflation, rose 0.3% for the month and 1.5% on a year-over-year basis which still falls well below the Fed’s 2% target. The Core PCE number excludes energy and food prices which tend to be more volatile. Since February of 2020, the M2 Money Supply, which is a broad measure of the amount of money available in the system, has increased more than 25%. From 2010 to 2019 the M2 Money Supply grew at an average of 5.8% per year1. The concern is that with a record amount of money available, falling COVID-19 cases, and a vaccinated public, further stimulus like the upcoming $1.9 trillion relief bill could serve as kickstart to rampant inflation. What we have seen though is that despite the increase in money available, the velocity, or the number of times that the money has been used to purchase goods or services, has fallen. For inflation to happen there needs to be both more money and higher velocity. This could be due in part to the fact that Americans are saving more than almost any other time in the last 80 years.

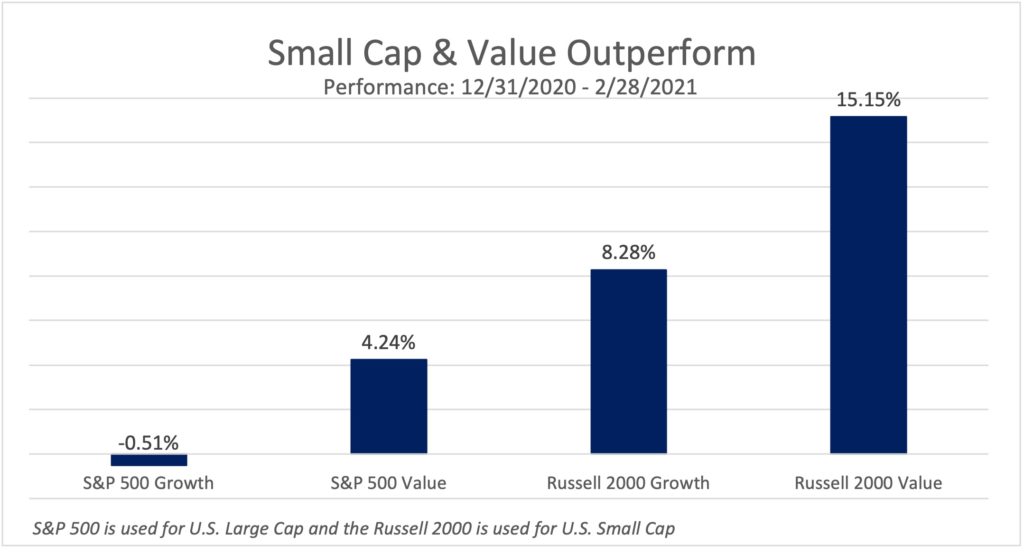

Year-to-date we have seen some of these concerns play out in the markets. The CBOE Volatility Index was up close to 40% from February 12th through February 26th. While the index remains elevated from a historical perspective, it is still well below the highs seen in February and March of last year. The Russell 2000, which is a broad measure for U.S. small cap companies, has handily outperformed the S&P 500. This is because the Russell 2000 has a greater exposure to cyclical industries such as Financials, Industrials, Real Estate and is substantially underweighted to the Technology sector which has been especially hard hit due to the rising yields.

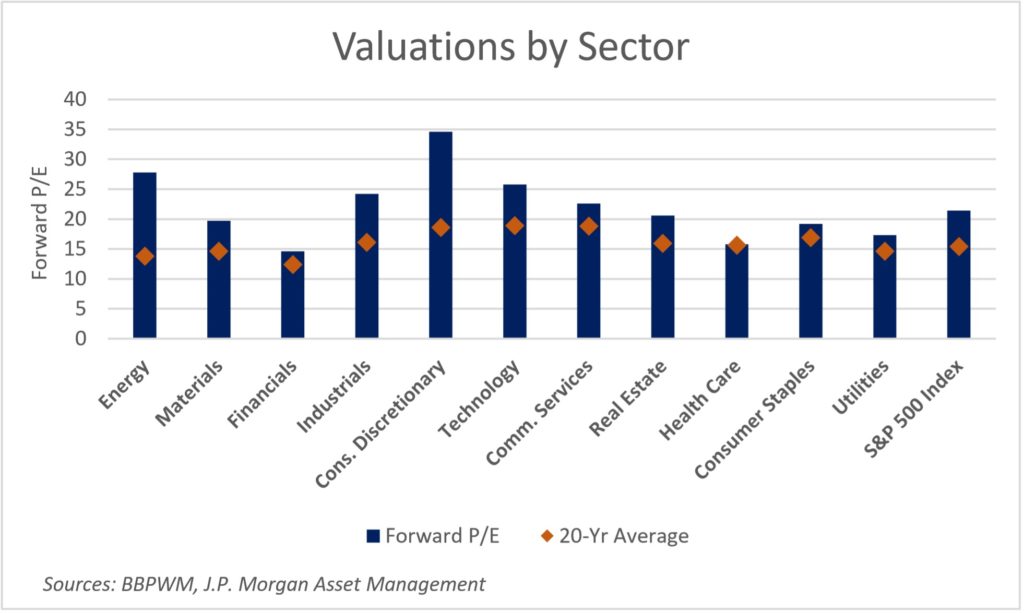

As of the end of February valuations remained elevated. High growth companies which have been the benefactor of depressed interest rates could continue to see their stock prices hurt if interest rates keep rising. These companies usually carry large debt loads used to finance their growth which becomes more expensive as rates rise. The lofty valuations of many of these companies compounds the problem as their earnings and/or future earnings are worth less with higher interest rates.

As we have stated in the past, we expect volatility to remain elevated as the market continues to grapple with above average valuations, rising rates, inflation concerns, and continued high unemployment. Based on current inflation, money supply and velocity, savings rates, and the Federal Reserve’s intention to let inflation run past its 2% target, inflation continues to remain a longer-term threat especially to fixed income investors. Others should remain cautious of the highly speculative stock boon that has been fueled by high amounts of stimulus and low interest rates. As Warren Buffet has been quoted as saying, “When the tide goes out, you find out who is swimming naked.” That of course is not to say that some of these companies will not turn out to be the next great innovators, but investors should be careful not to assume that valuations will not matter at some point.

1 WSJ – The Money Boom Is Already Here