Executive Summary

September has lived up to its reputation as the worst month for the stock market. The S&P finished down -4.65% for the month. Since 1945, the S&P 500 has averaged a -.56% decline. The first September of a new presidential administration is typically even worse, averaging a decline of -0.73% over the same time period1.

Congress avoided a government shutdown on October 1st providing temporary funding through early December, avoiding a repeat of the 35-day shutdown that spanned from December 2018 to January 2019, which was the longest on record. The larger looming risk markets have been dealing with is the suspension or increase in the debt ceiling. It is expected that that government will run out of money to pay its bills around October 18th. If the debt limit is not raised it would constitute default and could cause rating downgrades which would further raise the cost of borrowing and volatility for the markets. In addition, the U.S. government would not be able to pay salaries or benefits for federal and military personnel. Social Security, Medicare, Medicaid, and other benefit payments would also stop. Since its inception in 1939, the debt ceiling has been raised or modified 98 times which has allowed the U.S. to never default on its debt. Lifting the debt limit does not authorize any new spending but simply allows the U.S. to finance existing obligations2.

This comes as Democrats attempt to push through a $3.5 trillion-dollar economic package focused on climate change, income inequality, expanding Medicare, and education improvements along with a $1.2 trillion infrastructure bill which would funnel money towards improving roads, bridges, ports, and broadband. The cost of these packages would be partially funded through tax increases for both corporations and wealthy individuals, prescription drug policy changes, and other budgetary savings stemming from faster economic growth. While we expect the U.S. to raise the debt ceiling and avoid default, we expect volatility to remain elevated as partisan politics and grandstanding delay any agreement until the last minute.

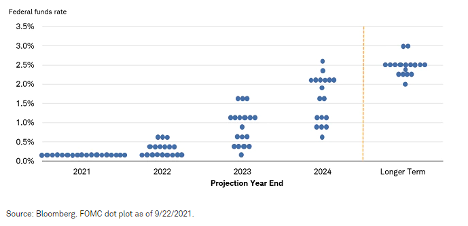

Federal funds rate

The above reasons aside, there are other reasons to expect volatility to remain elevated for the last quarter of the year. Federal Reserve Chair Jerome Powell indicated that the Fed may begin to reduce treasury and mortgage-backed asset purchases as early as November of this year likely finishing the process sometime in June of 2022. While he has remained adamant that tapering asset purchases is not directly related to interest rate increases, the infamous dot plot now shows officials are evenly split on beginning rate increases in 2022 and at least three increases by the end of 2023. During its last meeting in June the median projection indicated no rate increases until 2023. As of this writing the market is pricing at least one rate hike by September 2022.

The core Personal Consumption Expenditures (PCE) Index, the Federal Reserve’s preferred inflation measure, rose 3.6% on a year-over-year basis. The Fed anticipates core inflation for 2021 to be 3.7% and 2.3% in 2022 up from its June estimates of 3% and 2.1% respectively. The repeated belief is that inflation will be transitory but continued supply chain disruptions and shipping issues may keep inflation higher for longer. While all of this has been telegraphed by the Fed, any miscues on monetary policy will likely have negative ripple effects across markets.

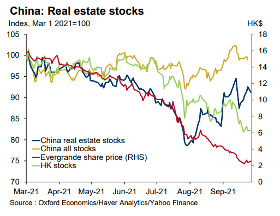

China: Real estate stocks

Additionally, investors are dealing with growing geopolitical risks like the potential collapse of Chinese property firm Evergrande as they digest comparisons to Lehman Brothers in 2008. Evergrande is the world’s most indebted property developer who failed to make interest payments on several bonds last week. Default has largely been anticipated for a couple years as the Chinese government began enacting policies designed to curb sky high real-estate prices. Larger concerns loom, however, about China’s struggles with excess corporate leverage. Managing high debt will be an ongoing issue as China’s nonfinancial corporate debt at 160% of GDP is higher than the advanced economy average, and rating agencies have flagged concerns about asset quality3.

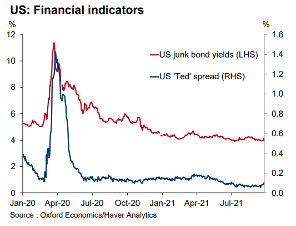

US: Financial indicators

So far most of the volatility has been confined to Chinese and Hong Kong markets. The TED spread, which measures the difference between three-month LIBOR and three-month treasuries, has remained stable along with U.S. junk bond yields. The TED spread is widely viewed as an indicator of credit risk in the market while non-investment grade yields tend to increase in times of distress and investor uncertainty.

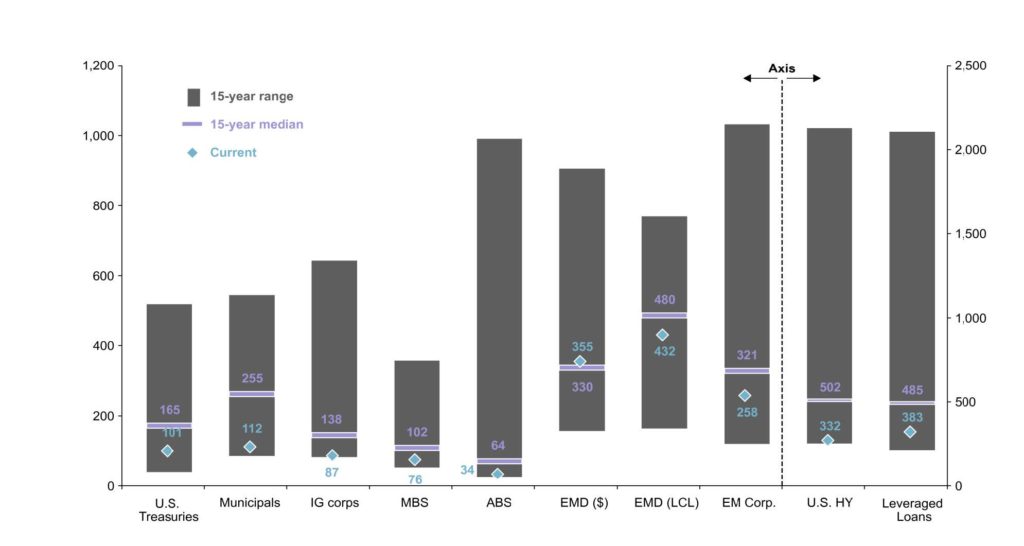

COVID-19 cases have been declining across the U.S. but continue to rise worldwide. As more people begin to congregate indoors heading into the holiday season, uncertainty surrounding the delta variant and booster shots could weigh on investor sentiment if restrictions reemerge. The estimated third quarter earnings growth rate for the S&P 500 is 27.6% which would be the third-highest earnings growth rate reported by the index since 20104. With such high expectations, disappointing earnings could lead to a repricing of stocks. Currently, the forward P/E of the S&P 500 stands at 20.55x which is still elevated from a historical perspective but down from its recent highs hit earlier this year. Fixed Income markets could be viewed as even more expensive. Even with the recent rise in yields, current real yields, after factoring in inflation, are steeply negative. Many spreads-to-worst across fixed income sectors are at or near their lowest levels in 15 years. Spread-to-worst measures the difference between the yield-to-worst of a bond and the yield-to-worst of a U.S. treasury with a similar duration. Spread is the additional compensation that investors require for taking on additional risk, whether that’s duration risk (risk associated with changing interest rates) or credit risk (risk of loss resulting from default by the borrower). Simply, investors are requiring less compensation for taking on additional risk across fixed income sectors. Earnings disappointments, unexpected inflation, and/or slower than expected economic growth may cause increased volatility in both equity and fixed income markets.

Spread-to-worst across fixed income sectors

Basis points, past 15 years

This seemingly endless wall of worry always exists. Valuation concerns, geopolitical risks, slowing growth projections, runaway inflation, earning revisions, monetary policy missteps among any number of other risks often look to derail even the best long-term investors. We forgo current consumption to invest for the future benefits that it provides. Those benefits would not be available without taking risk. This is not to say that the present risks do not matter. It is a reminder that these risks are ever present and are they are the reason we can earn the returns over time to fund our future goals. Managing that risk by making sure the amount of risk you are taking is aligned with your risk tolerances and objectives will better ensure you reach those goals. As always, we appreciate the trust you place in us, and if you would like to review your portfolio, objectives, life changes, or future needs please do not hesitate to reach out.

1 – Forbes: Why Stocks May Suffer In September

2 – New York Times: Explaining the U.S. Debt Limit and Why It Became a Bargaining Tool

3 – Oxford Economics: Evergrande matters, but it’s not a ‘Lehman moment’

4 – FactSet Earnings Insight – September 24, 2021