Executive Summary

For the fourth quarter of 2020 GDP grew at an annual rate of 4%, which was a touch lower than most projections. For 2020 overall, GDP fell 3.5% in annual terms. The International Monetary Fund (IMF) recently revised up their global growth estimates for 2021 to 5.5% and 4.2% for 2022, citing ramped up vaccine rollouts and additional monetary and fiscal policy support. For the United States specifically they are estimating 5.1% GDP growth in 2021 and 2.5% in 2022.

Historically low interest rates and lack of inventory has continued to push existing home prices higher. The S&P CoreLogic Case-Shiller Home Price Indices track residential real estate price changes nationally and across 10 and 20 of the most densely populated cities. On a year over year basis the 10-city and 20-city indexes were up 8.74% and 9.07% respectively. The National Index was up 9.49% year over year which corroborates the evidence from other housing market reports that demand has strengthened more in smaller urban, suburban, and rural areas than in large metro areas, partly due to COVID1.

The Conference Board Leading Economic Index® increased to 109.5 albeit at a slower pace than months prior. The index is comprised of 10 economic variables that have generally signaled changes in the business cycle. In general, readings above 100 are positive, indicating economic growth and readings below 100 are indicative of weakening economic factors. While the reading was positive, the slowing rate of change, a 0.3% increase in December, 0.7% increase in November, and 0.9% increase in October, is illustrative of a deceleration in economic growth as the country continues to battle with the ongoing effects of the pandemic.

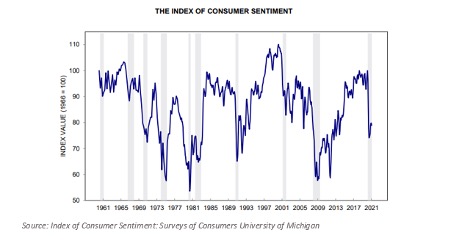

Consumer confidence continues to remain near 2020 recession lows. These surveys attempt to measure consumers current sentiment on the economic backdrop, their projected spending plans and financial situations, and expectations of stock prices, interest rates, and inflation.

This coincides with what we have seen from the labor market with unemployment still hovering around 6.7% and over 18 million individuals who have claimed some form of unemployment insurance for the week ending January 9th, an increase of 2.3 million from the previous week. As a comparison, there were 2.1 million weekly totals during the same time last year2. Looking forward however, expectations for future growth and spending continues to improve as vaccine distribution picks up and stimulus remains accommodative.

Through the end of January just over a third of the companies in the S&P 500 have reported their earnings for the fourth quarter of 2020. According to FactSet, 82% of those companies have reported a positive EPS surprise and 76% have reported a positive revenue surprise. As of now the projected earnings decline for the S&P 500 is -2.3%, compared with an estimated -9.3% at the end of 2020. Companies are beating estimates by wider margins than usual. In total, companies are reporting earnings that are 13.6% above estimates, which is above the 5-year average of 6.3%3. Looking ahead analysts have continued to revise estimates for first-quarter 2021 earnings higher. As of now the forward P/E for the S&P 500 stands at 21.71x which is still high from a historical perspective. In fact, most of the standard stock market valuation measures signal overvaluation except when you compare the earnings yield of the S&P 500 to current bond yields.

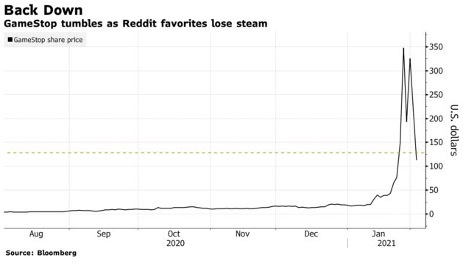

Finally, I would be remiss if I did not touch on the recent events surrounding GameStop, AMC, and some other heavily shorted stocks last week as they rose at a parabolic rate creating concern and volatility across the markets. When a stock is shorted, the investor must first borrow the shares, at which point they will then sell the shares in the market with the intention of profiting if the stock price drops. If the stock price rises short sellers will incur losses and if the stock price rises enough the short sellers will be forced to buy back the stock and return the borrowed shares. This is because shorting a stock is considered a leveraged position and there is theoretically the potential for infinite losses as there is no limit on how much a stock price can rise.

Last week retail investors grouping on chatrooms and social media targeted GameStop to buy, which at time was the most heavily shorted stock in the market. Their intention was to cause a short squeeze. A short squeeze is when a stock is bought with the intention of raising the price so that short sellers must buy back the stock creating even larger gains. As GameStop’s shares continued to rise, short sellers were forced to buy back a portion of their shorted shares which fueled further increases. As the stock gains continued, more and more people joined pushing prices still higher. Through January, hedge funds, the institutions that are mostly short GameStop, lost over $12.5 billion dollars. The market then shifted focus to other heavily shorted names such as AMC, Koss Corporation, Express, BlackBerry, and Bed Bath & Beyond among others rocketing those stock prices higher in similar fashion.

Last Thursday, in a seemingly unprecedented act, Robinhood and other brokerages halted trading on many of these securities only allowing liquidation trades which meant that people could only sell their shares or options. Data released last week from Ortex indicated that short-sellers have loss about $70 billion on their overall short positions on U.S. firms year to date. New fears about the risk of financial contagion if hedge funds were forced out of business and continued concerns about the excessive optimism in the retail market have recently driven volatility higher.

We have had a bit of a reprieve with the number of daily COVID-19 cases falling over the past month but with new variants of the virus, ongoing vaccine distribution difficulties, and extended lockdowns we continue to expect market volatility to remain elevated. Market valuations continue to look stretched, perhaps pricing in a faster recovery than some economic data might suggest. With all that is happening it’s important to remain focused on your long-term goals and objectives. Many times, investor behavior is more important than the individual components of a portfolio. Speaking with an advisor and reviewing your allocation will help put your portfolio in perspective and keep you on track to achieve your goals.

1 Ned Davis Research U.S. Daily Economic Perspectives

2U.S Department of Labor – Unemployment Insurance Initial Claims

3FactSet Earnings Insight – January 29, 2021