In 2015, congress passed a law that would eliminate some of the more favorable Social Security strategies. Anyone born after January 1st, 1954, would no longer be able to use the restricted applications or file and suspend methods for claiming.

The removal of these practices left people with few options for increasing their lifetime benefits. When you claim and how long you live will ultimately be the biggest factors in determining your potential lifetime benefits.

Timing is everything

The calculation of your Primary Insurance Amount (PIA) determines your benefits payable at Full retirement Age (FRA). The FRA is a moving target and depends on your date of birth. As the years are moving along, the Full Retirement Age is getting older. For instance, anyone born after 1960 will have an FRA of 67.

On top of that, a person may claim as early as 62 and as late as age 70. Claiming earlier or later will change your benefit.

Claiming earlier than FRA comes with a reduction of about 6.66% per year. So, someone claiming at age 62 would see their benefit reduced by about 25%.

On the flip side, those that delay claiming past FRA will see an annual increase of 8% per year up to age 70. So, delaying the maximum time could lead to a 32% increase in one’s benefit.

The Breakeven Point

Of course, when you should claim almost entirely depends on how long you live. Because, while there is a benefit to waiting there is also a cost. That cost is forgoing years of collecting benefits and instead using portfolio dollars to fund retirement.

Example:

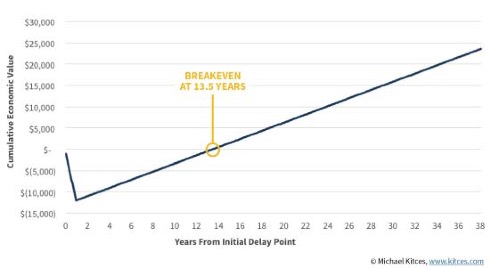

A 66-year-old retiree who is full retirement age and is currently entitled to a benefit of $1,000/month. He could begin that $1,000/month payment today or delay a year in order to receive an 8% delayed retirement credit, boosting his benefit to $1,080/month, but forgoing $1,000/month x 12 months = $12,000 in order to get that $80/month boost. Thus, the question arises: how long does it take to recover the $12,000 shortfall with an extra $80/month thereafter? The answer: it takes about 13 years to break even, as shown above in Figure 8 (below).

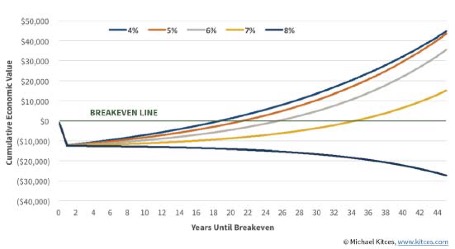

Of course, the real cost to delaying in this situation is known as opportunity cost. Because in the situation above not collecting the $12,000 would most likely means that the individual must get that $12,000 from their portfolio. This is $12,000 that will not remain invested. So, we then need to calculate the breakeven point using an assumed growth rate. At a mere 4% growth rate, the breakeven point extends to 18 years and at 6% it extends to 25.

Ultimately, there are three factors that drive the relative benefit of delaying Social Security.

Delaying Social Security works best when growth rates are low, inflation is high, and life expectancy is long. On the flip side, delaying is not as effective when returns are good, inflation is modest, and retirement, sadly turns out to be short.

Conclusion

Deciding when to collect your benefits involves a lot of unknown factors and can be overwhelming. If you would like some guidance we are here to help. Give us a call at 610-825-3540. Look out for Part 2 when we examine couples claiming strategies.