Blue Bell Private Wealth Management

- Mutual fund annual distributions can create a major “tax drag” on your real after-tax return with annual fund tax costs potentially two times the annual fund expense ratio. Most ETFs never pay out capital gains and you determine when to take a capital gain by selling your shares of the ETF.

- Mutual funds distribute capital gains at the end of every year while ETFs rarely, if ever, have capital gains they are required to distribute to shareholders, allowing the shareholders to control when they take capital gains at the time of sale.

- ETFs are bought and sold on an exchange and therefore do not have to meet shareholder redemptions by selling securities. If the ETF does need to sell shares to meet an index rebalancing, the shares they sell will likely not have any capital gains because of a security creation/redemption process allowing for “in-kind” exchanges of shares.

Need to speak with an advisor, click here to schedule a 20-Minute Consultation on Mike’s calendar now.

Intro:

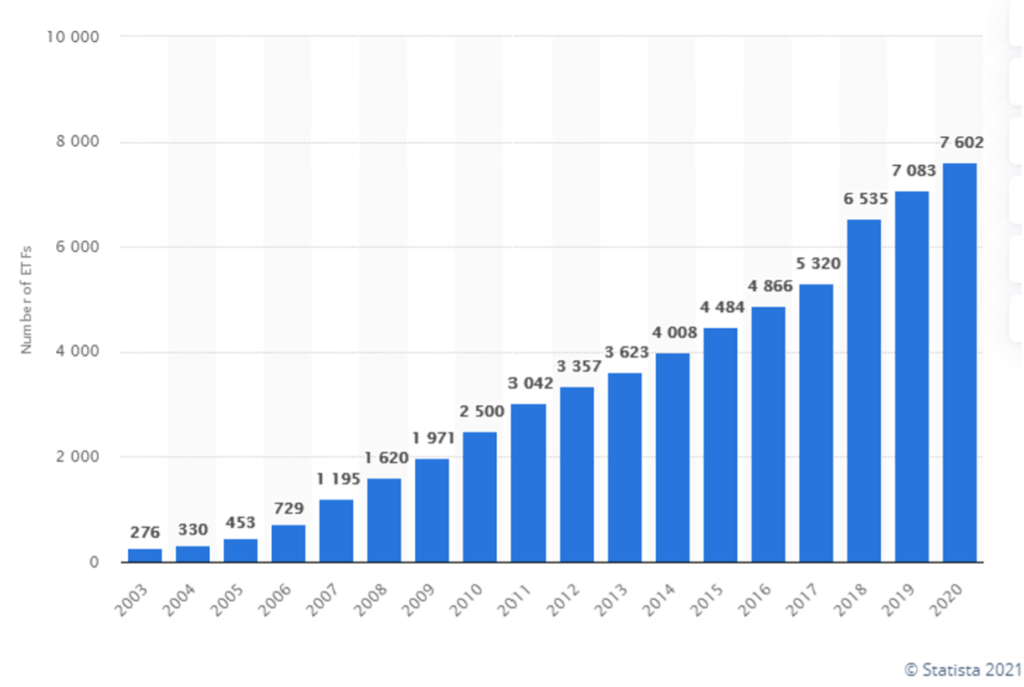

The first Exchange Traded Fund (ETF) was listed on the American Stock Exchange (Amex) in 1993 creating a new investor revolution and a big win for all investors. When I started as a Financial Advisor in 2005, there were 453 ETFs. Today, there are over 7,602 publicly traded ETFs in all shapes, sizes, and varieties.

Most ETFs are “indexed” investments that own/track the underlying securities of a particular index like, the S&P 500, DOW 30, NASDAQ 100, or Barclays U.S. Aggregate Bond Index (to name a few examples). Like the growth of ETFs, various companies have been creating new indexes or baskets of securities to track. Today, if you have an idea you want to invest in, there is most likely an ETF you can buy to gain instant diversification to a country, sector, industry, or type of security.

What’s the big deal? Not only are ETFs a very low-cost way to gain diversification and build your core portfolio, but they are an incredibly tax efficient way to invest in your taxable investment accounts. Unlike mutual funds that have capital gains distributions at the end of every year, ETFs rarely if ever pay capital gains from the fund.

You can plan the timing of capital gains by when you choose to sell the ETF. At that point, it is just like owning an individual stock. If you’ve held the ETF for over one year, you’ll pay Long-Term Capital Gains. Gains sold under a year; you’ll pay at your ordinary income tax rate. If you have a capital loss, you can use the loss to offset other gains or potentially deduct up to $3,000 against your other income for that tax year.

ETF tax efficiency is a bigger deal than most people recognize. After all, it’s how much return you get to keep after-taxes that should matter the most to you. Nobody likes paying a big tax bill on mutual fund capital gains that were reinvested in the fund especially if the fund drops the following year. In my opinion, that’s a gross waste of your resources and an inefficiency that shouldn’t be happening.

Without going to far into the diminutive details of the tax rules that allows ETFs to create this tax efficiency, this article will explore how it works and the benefits to investors. The bottom-line, don’t let taxes be the real drag on your portfolio performance.

Number of exchange traded funds (ETFs) worldwide from 2003 to 2020 (Source: Statista)

Tax Drag Hurts:

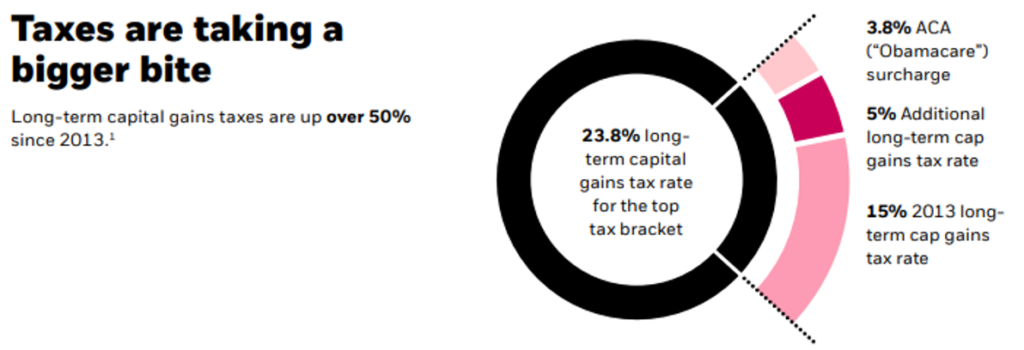

Paying additional taxes hurts everyone’s real after-tax portfolio return. If you’re in a high tax bracket, these taxes can be significantly more than just an annoyance. For higher income earners, long-term capital gains taxes have increased over 50% since 2013.

Keep more of what you earn (Source: BlackRock/iShares ETFs)

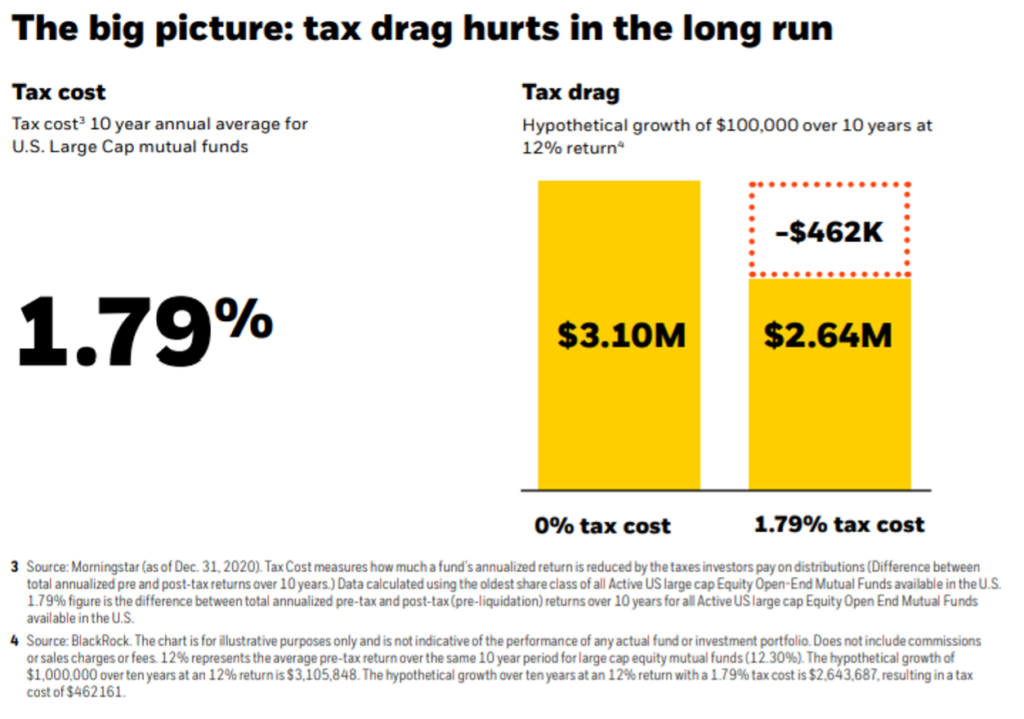

According to BlackRock, the provider of iShares ETFs and BlackRock Funds, the average annual “tax drag” of U.S. Large Cap mutual funds represents a cost to shareholders that own shares in a taxable account that is 2X the average annual fund expense ratio. Meaning your losing far more money to unnecessary taxes than you’re paying the manager to manage the portfolio.

Source: ©2021 BlackRock, Inc

Remember that these mutual fund tax distributions are happening whether you sell shares or not. This is just one of the major inefficiencies of owning mutual funds, especially in a taxable account. I would hate to be the advisor that has to explain to a client why they owe so much tax when they didn’t sell their shares and reinvested back into the fund. This effect was especially noticeable after 2019 fund distributions and the early 2020 pandemic market crash.

Our job as advisors is to make sure our clients are utilizing all their economic resources in the most efficient ways possible. Paying unnecessary taxes is something that can be easily avoided by legal means. We all must pay our fair share, but we don’t have to plan and invest in ways that are detrimental to our own financial wellbeing.

Given the time-value of money and exponential compounding overtime, we’re not taking about couch change. All these inefficiencies add up to big money overtime. Care is always needed with portfolio management to make sure you are investing prudently and efficiently toward your personal objectives.

Source: ©2021 BlackRock, Inc

As you can see above in BlackRock’s hypothetical example of a $1,000,000 investment (their image drops a few zeros at the end), tax drag alone would have accounted for lost capital to the shareholder of $462,000 over the 10-year timeframe. If the example was for $100,000, the tax drag loss would be over $46,000. Clearly, investors should not be taking these inefficiencies lightly.

How can ETFs avoid the need to pay capital gains?

Both ETFs and mutual funds have to payout capital gains to shareholders by law after selling shares for a gain for either tactical reasons or to meet shareholder redemptions. Let’s take a quick look at how ETFs handle these transactions.

First, most ETFs are indexed investments with very low position turnover. With that said, they are still much more tax efficient than their Indexed mutual fund relatives. This is due to how ETF shares are created and redeemed.

When a mutual fund investor redeems shares directly from the fund provider, the fund must sell securities to raise cash to meet the redemption. This is another mutual fund inefficiency that makes the funds highly reliant on fund flows in or out of the fund.

When an ETF investor wants to sell shares, they sell it on the open market to another investor just like a stock. The seller must handle the tax consequences, but there is no impact on the fund. Pretty straight forward and clean.

Things get a bit more complicated for ETF administration when dealing with their “authorized participants” or “APs.” These are organizations that have the right to create and redeem shares of an ETF. Not to worry though. When an AP redeems shares, the ETF issuer pays the AP “in kind” with shares of the underlying holdings of the ETF. No sales, NO CAPITAL GAINS to the ETF.

The ETF strategically plans the shares to give the AP to reduce the taxes of the ETF and get higher after-tax returns for the ETF shareholders. ETFs, like funds, are constantly buying and selling shares. The ETF can replace shares at higher and higher prices over time leading to more tax efficiency in the future.

One caveat is that this does not work equally as well across all ETFs. You should know the potential for capital gains when investing in bond, commodity, futures, or master limited partnership (MLP) ETFs that will have higher turnover of the underlying portfolio. Depending on your tax situation, owning individual securities in these areas will likely be more tax efficient. Given the scope of this article, I’m not going to dive deeper into the tax efficiency of all available ETF security ownership types.

For more, check out this brief clip with Dave Nadig from ETF.com on CNBC.

The bottom-line is that ETFs broadly are a significantly more tax-efficient way to invest and get instant diversification to a segment of the stock market or broad-based exposure. With over two decades of existence, I firmly believe ETFs have proven themselves to be great investment vehicles and should be a foundational part of most investor portfolios.

Schedule a 20-Minute Consultation with Mike, here.

Mike Weber, CFP®

484-221-5408

Blue Bell Private Wealth Management is an independent, fee-only Registered Investment Advisor providing financial planning, investment and wealth management services for all generations.