The main purpose of saving and investing is to accumulate enough assets that will both supplement your income and allow you to maintain a comfortable lifestyle in retirement. Doing so requires discipline, patience, and most importantly, a plan.

However, once you’ve successfully reached retirement that does not mean that the planning stops. You need to have what we call a “withdrawal strategy” that will cover your income needs while being as tax efficient as possible. This blog will serve as a guide on how certain withdrawals can impact your taxes in different ways.

Types of retirement accounts

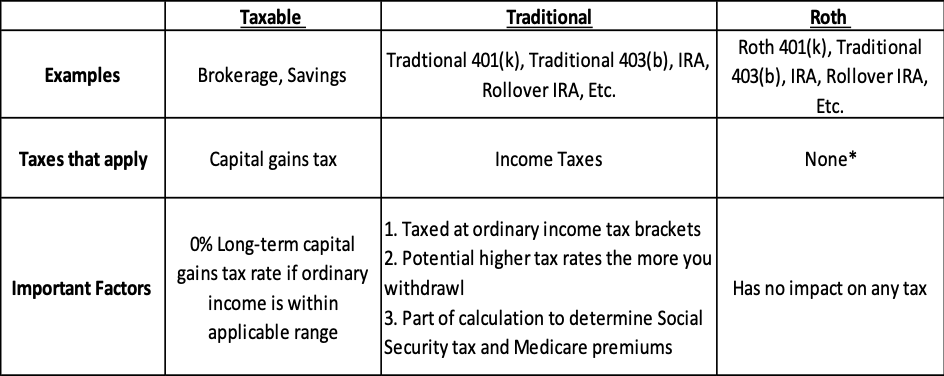

The first thing we need to cover is the three different types of accounts that you will be withdrawing from. They are taxable, traditional, and Roth accounts. Below is a table that shows the examples and how they are taxed:

*A 10% penalty may apply if you are under the age 59.5. In addition, the 401(k) and 403(b) may have plan limitations that would prevent a withdrawal prior to a triggering event such as death, termination, disability, or retirement.

Finding the right Strategy

First and foremost, you want to find a withdrawal strategy that covers your needs and lasts you through retirement. Many experts recommend not withdrawing more the 4-5% of your assets per year. However, everyone’s situation is different so working with an advisor may help you here.

After you know what you need you must figure out where you are going to take the money from. There are two types of withdrawal strategies, traditional and proportional.

Traditional

This strategy takes the withdrawals in this order:

The idea behind the traditional is to defer paying the taxes on your traditional assets and allowing your Roth accounts to continue growing tax free.

To help get a clearer picture of how this could work, let’s look at a hypothetical example:

Joe is 62 and single. He has $200,000 in taxable accounts, $250,000 in traditional 401(k) accounts and IRAs, and $50,000 in a Roth IRA. He receives $25,000 per year in Social Security and has a total after-tax income need of $60,000 per year. Let’s assume a 5% annual return.

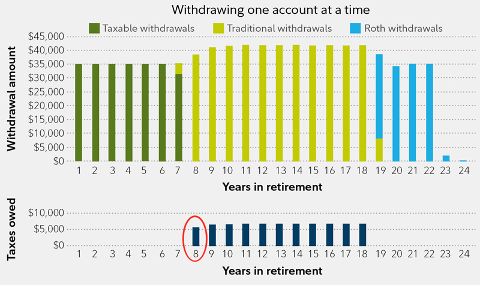

If Joe takes a traditional approach, withdrawing from one account at a time, starting with taxable, then traditional and finally Roth, his savings will last slightly more than 22 years and he will pay an estimated $74,000 in taxes throughout his retirement.

For illustrative purposes only. Assumes 5% annual rate of return. Does not consider state and local taxes. All values in real terms and all tax rules assumed to be 2018 tax rules for entire time period.

Note that with the traditional approach, Joe hits an abrupt “tax bump” (see red circle in chart) in year 8 where he pays over $5,000 in taxes for 11 years while paying nothing for the first 7 years and nothing when he starts to withdraw from his Roth account.

The traditional strategy is most effective when you only have taxable and traditional assets.

Proportional Withdrawals

If you are someone with multiple types of accounts a proportional withdrawal strategy may make more sense.

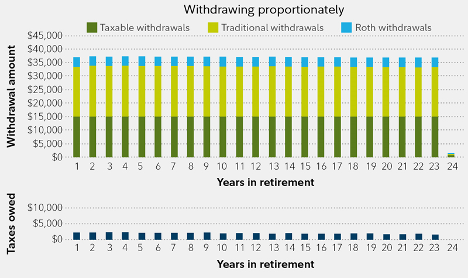

For a proportional strategy, an investor would withdrawal from every account based on that account’s percentage of their overall savings.

The effect is a more stable tax bill over retirement, and potentially lower lifetime taxes and higher lifetime after-tax income. Let’s look at the same example from above using a proportional withdrawal strategy:

*Assumes 5% annual rate of return. Does not consider state and local taxes. All values in real terms and all tax rules assumed to be 2018 tax rules for entire time period.

This approach provides Joe an extra year of retirement income and costs him only $46,000 in taxes over the course of his retirement. That’s a reduction of almost 40% in total taxes paid on his income in retirement

By spreading out taxable income more evenly over retirement, you may also be able to potentially reduce the taxes you pay on Social Security benefits and the premiums you pay on Medicare.

Conclusion

Everyone’s situation is different, and the right strategy will be dependent on a multitude of factors including types of accounts, income tax brackets, and life expectancy.

If you would like to sit down and figure out which strategy is right for you, we provide complementary income planning consultations. Just schedule a call with us using the speak to an advisor tab or reach out at 610-825-3540.