Get the most out of your employee stock options (Part 1)

Stock options are a popular way to attract and retain employees by giving them a sense of ownership in the company. Stock options, which give you the right to buy shares at a pre-determined price at a future date, come in two different forms. The major difference between these forms is how they are taxed. It is important to understand your stock options and have a plan for managing them.

Option Basics

There are a few terms that you need to understand before we go into the different types and how they are taxed. Here are some basic explanations:

Non-Qualified Options (NSO’s)

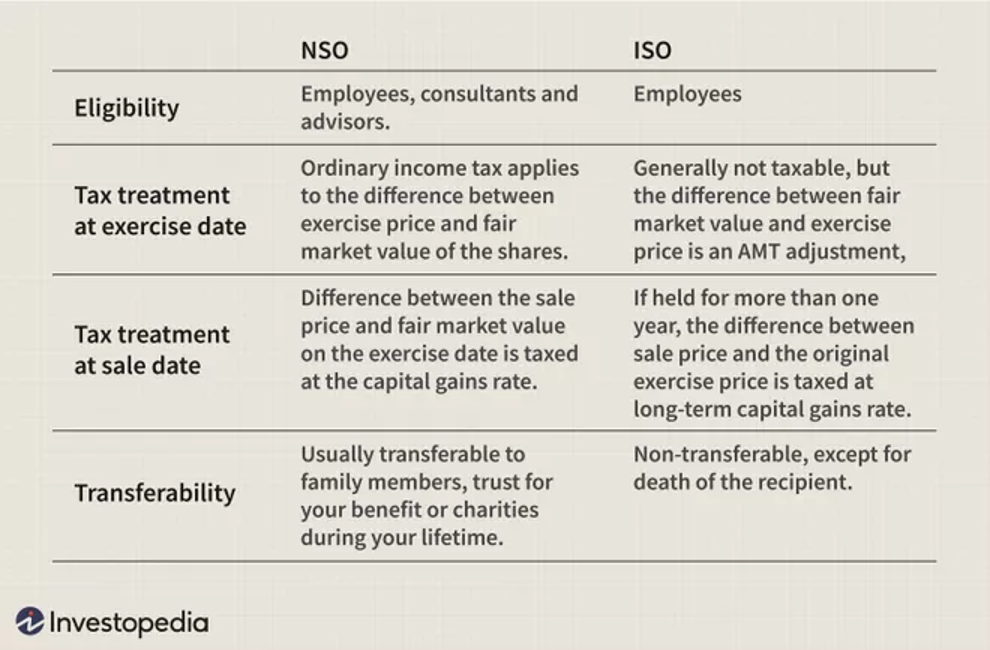

The more common type of employee stock options is the Non-qualified Stock option or NSO. NSO’s are taxable as income when exercised.

For example, if you were granted NSO’s with an exercise price of $10 and the market price of the stock is $30 when you exercise them, you pay income tax on the $20 ($30-$10).

When you subsequently sell the shares, any further increase in the sale price is subject to capital gains tax (short-term for less than a year and long-term if more than a year). For example, if you exercise your options at $30 and sell them later for $50 the difference ($20) will be taxed at long-term capital gains tax rates (assuming you held for one than one year after exercise).

Incentive Stock options (ISO’s)

Incentive stock options (ISO’s) are usually given to key employees and can be more advantageous due to the way they are taxed. When an ISO is exercised it is not a taxable event.

Instead, when you sell the shares, the difference between the grant price and the sale price is taxed at long-term capital gains rates.

To qualify for this preferential tax treatment, two requirements must be met. The ISO’s must be held for 2 years from the date they were granted and one year from the date they were exercised.

Otherwise, a “disqualifying disposition” occurs and the difference will then be taxed at ordinary income.

There are a few other things to consider when planning around ISO’s.

One is that that certain high-income earner may be subject to Alternative Minimum Tax (AMT) upon exercise, so it is important that you check in in with your tax preparer.

The other, is that most ISO’s must be exercised within 10 years of the grant date. Otherwise, they may become worthless.