Blue Bell Private Wealth Management

Giving to charity not only makes a positive philanthropic impact, but it can also have a positive impact on your taxes. It’s a rare win-win situation in today’s world.

This is because charitable donations can be used as deductions against your taxes (assuming you itemize deductions). It is important when considering donating to charity that you look at your entire financial situation. This way you can optimize your giving and the deduction you receive. Here are a few strategies that can be used when donating to charity.

- Donating appreciated stock

Donating appreciated stock is the process of transferring securities selected by you to the charity. The charity then sells the shares and uses the proceeds as they see fit. Donating stock accomplishes three main objectives:

- Gives funds to a charity of your choosing

- Helps you avoid capital gains tax on highly appreciated holdings

- Provides for an income deduction of up 30% of your adjusted gross income and allows you to carryover for five years if your deduction exceeds AGI limits each year

This strategy can be great for people that have low-cost basis and want to avoid paying capital gains taxes.

Donating appreciated stock may be a financially effective way to satisfy your philanthropic endeavors. However, everyone’s situation is different so always discuss your plans with both your advisor and your tax preparer before moving forward.

- Set up a charitable remainder trust

A charitable remainder trust otherwise known as a CRAT or CRUT allows you to do the following:

- Give money to a charity or charities or your choosing

- Receive a deduction for any asset put into the trust

- You or a beneficiary of your choosing receive income for a period of time (usually life) from the trust

To create a charitable remainder trust, you will need to transfer assets into an irrevocable trust with a charitable remainder. For example, you can transfer a rental property you own into a charitable remainder trust. Once your trust is funded with assets, either you or your named beneficiary will receive annual payments from the trust. Then, when you pass away, the remainder of the assets in the trust will be donated to the charity you have named.

Charitable trusts are great for those who are not ready to give up the income form their assets but wish to ensure select charities receive the remained when they pass.

Charitable trusts can be very complex and need to be created by a licensed estate attorney, so it is important to meet with one when considering this strategy.

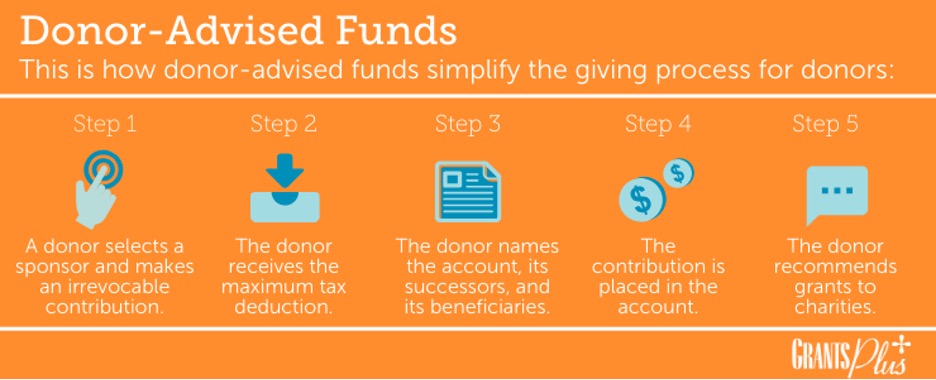

- Set up a Donor Advised Fund

A donor-advised fund is a philanthropic giving vehicle in which an individual deposits contributions without choosing a specific recipient right away. When the donor decides on a recipient, they can send the money from the account to the nonprofit organization as a grant.

Donors can contribute to their DAF account as frequently as they’d like. When they deposit assets into the account, they receive the charitable tax deduction immediately without the pressure of selecting a recipient organization right then.

Once the donor contributes assets into the DAF, the sponsoring organization has legal control of the funds. However, the donor (or the donor’s representative) holds the advisory privileges, so they advise the sponsor to direct grants to specific charities.

DAFs can be a great tool for those who know they want to give to charity but are either not set on which charity or the timing of the gifts.

- Qualified Charitable Donations (QCDs)

QCD’s are a great tool for those above the age of 70.5. Qualified charitable donations (QCDs) can allow further tax benefits to individual retirement accounts (IRAs). At the age of 72, regardless of what you desire to do, the IRS requires traditional IRA owners to take out an annual withdraw called a required minimum distribution (RMDs) from their IRA. RMDs can become a burden, given that it is a source of taxable income, causing an individual to be pushed into a higher tax bracket. In addition to paying a higher tax rate, entering a higher tax bracket can have negative affects on Social Security payments and Medicare benefits.

RMDs can be used to help lower your taxes with a QCDs. Starting at the age of 70 ½, couples can make a QCDs up to $100,000 each per a year. The donation can go to one or multiple operating charities. This excludes donor-advised funds, all donations must be given to a qualified charitable organization. The donation comes directly from the IRA and can include all or a portion of the RMDs. By donating directly out of the IRA, the RMDs is no longer included as adjusted gross income (AGI) on a tax report. By reducing the total amount of taxable income, QCDs can provide additional tax benefits when compared to a standard cash donation. QCDs are not an annual tax deduction, but rather a way for the RMDs to be excluded from taxable income.

If you are considering giving money to charity it is important to speak with a financial planner first. We can help you assess your entire situation and make sure your giving is optimized. Schedule a call with using the speak to an advisor button.