Optimizing Tax Planning and Retirement Strategies for High-Earning Young Professionals

*To ensure confidentiality, all names in this document are fictitious to the best of our knowledge.

This case study examines the financial situation of a young couple, both 28 years old, who are high earners with a combined annual income of approximately $450,000, including bonuses. The couple sought the assistance of a registered investment advisor to help them with investments, retirement planning, and tax planning. This case study highlights the advisor’s recommendations and strategies to maximize tax efficiency, significantly increase tax-free retirement savings, and plan for future healthcare expenses.

Client Profile

Age: Both 28 years old

Combined Annual Income: Approximately $450,000 (including bonuses)

Expenses (including housing): $80,000 per year

Employment: Sally works at a technology company. Scott has reviewed numerous retirement plan offerings and immediately identified that the plan offers a Mega-backdoor Roth IRA

Objective

- Maximize tax efficiency and retirement savings.

Recommendations

- Implement a Mega Backdoor Roth IRA strategy for Sally.

- Establish Backdoor Roth IRAs for both clients.

- Optimize Health Savings Account (HSA) contributions for tax advantages and future healthcare expenses.

- Create a comprehensive financial plan with visual cash flow mapping.

Analysis and Recommendations

Mega Backdoor Roth IRA

The advisor identified an opportunity for Sally to take advantage of the Mega Backdoor Roth IRA strategy offered by her employer. Sally can contribute the maximum pre-tax amount of $22,500, with her employer matching $11,250, totaling $33,750. However, in 2023, a total contribution limit of $66,000 is allowed. Therefore, the advisor recommended that Sally contribute an additional $32,250 after-tax to the plan, which her employer would immediately roll into a Roth IRA. This strategy enabled Sally to contribute a total of $32,250 to a Roth IRA, significantly increasing her retirement savings and providing excellent tax planning.

Backdoor Roth IRAs

Since the couple did not have traditional IRAs, the advisor recommended utilizing the Backdoor Roth IRA strategy. In 2023, they were able to contribute $6,500 each, totaling $13,000. When added to the Mega Backdoor Roth IRA contribution, the couple managed to contribute a total of $45,250 to Roth IRAs in just one year. Furthermore, the advisor helped them contribute an additional $12,000 for the missed 2022 year, resulting in a total of $57,250 in Roth IRA contributions.

Maximizing HSA Contributions

Upon reviewing the couple’s tax return, the advisor noticed that they had withdrawn money from their Health Savings Account (HSA). Recognizing the tax advantages of HSAs, the advisor recommended that the couple maximize their HSA contributions instead. By contributing the maximum allowable amount to their HSAs, the couple could benefit from a tax deduction while also planning for future healthcare expenses. Any gains on the HSA investments would be tax-free, providing a combination of tax-deductible contributions (similar to a traditional IRA) and tax-free growth (similar to a Roth IRA).

Cash Flow Mapping and Financial Confidence

To provide the couple with a clear understanding of their financial situation and aid in their investment decisions, the advisor created a visual cash flow map. This map visually depicted their income, expenses, savings, and investment allocations. By having a comprehensive overview, the couple gained confidence in their financial plan, realizing they were saving more than necessary. The visualization helped align their goals and provided a foundation for effective decision-making.

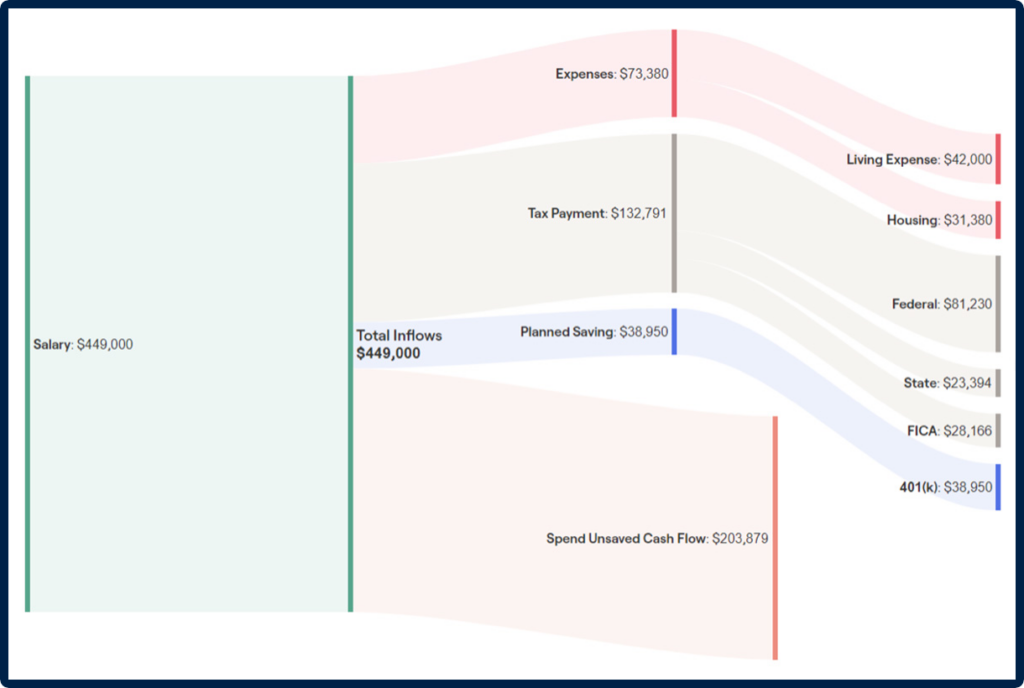

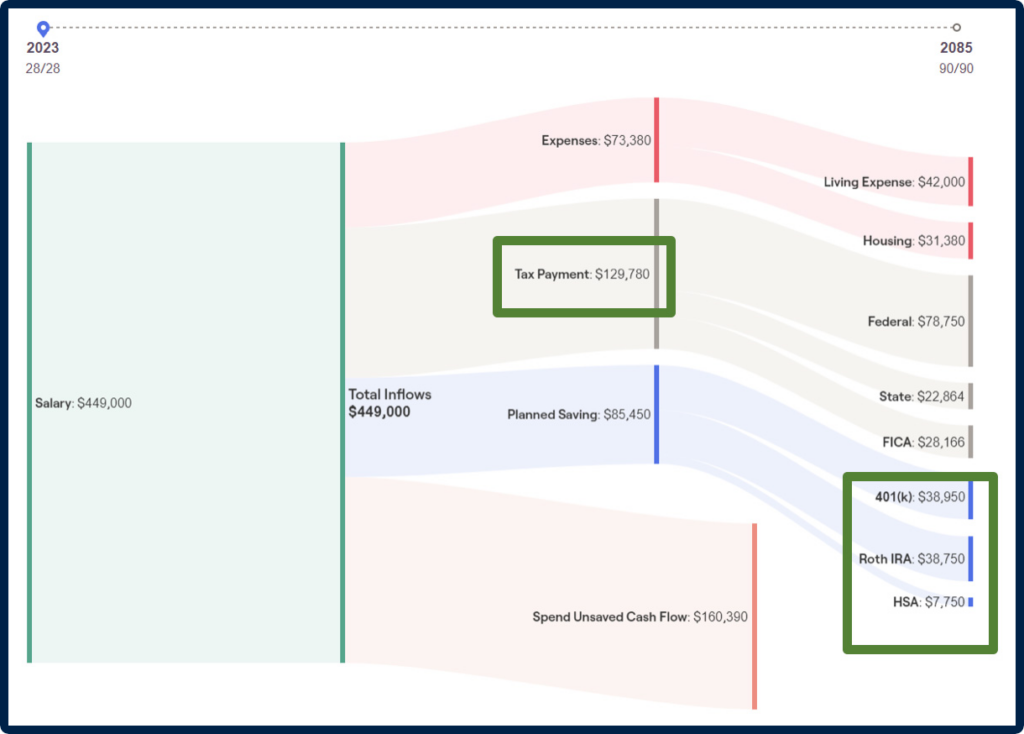

Recommended:

The recommended strategy mapped out above compared to what they would have done (mapped out below), reduced overall taxes by over $3,000 while increasing contributions to Tax free Roth and Health Savings accounts by over $46,000.