In this case study, we explore our strategy for assisting a couple within a decade of retirement, often referred to as pre-retirees. These individuals have been diligently saving for their retirement while simultaneously supporting the education of their two children. This dual financial responsibility brought significant stress, as they were concerned about their ability to retire on time. However, now that their children have completed their education and moved out, the couple is eager to refocus their efforts on ensuring they are back on track for retirement.

Client Profile:

- Age: Both 55 years old

- Target Retirement Date: 65 for both

- Assets:

- Taxable: $200,000

- After-tax: $250,000

- Pre-tax: $550,000

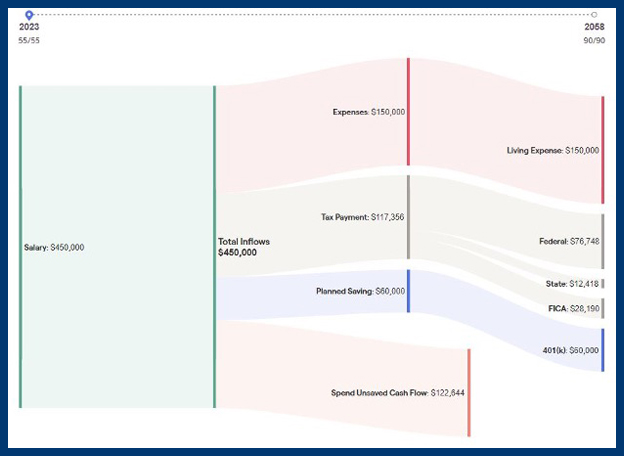

- Income: $450,000

- Expenses: $150,000

- Savings: Both are maximizing their 401(k)s with employer matches of 3%

The couple’s primary goal is to maintain their current lifestyle in retirement, implying that we do not anticipate a significant reduction in their expenses. After inputting all relevant data into our planning system, the initial results are as follows:

- Current Financial Status:

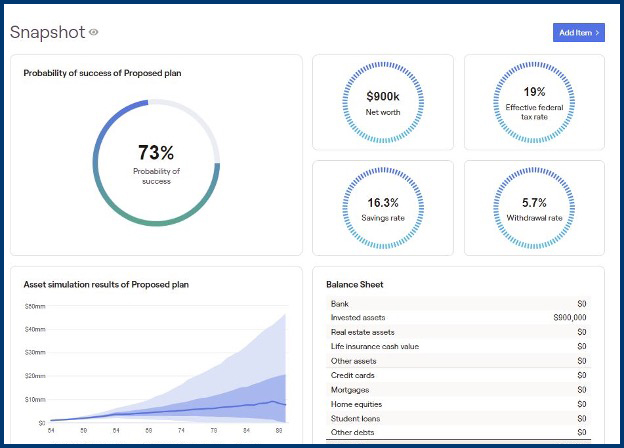

- The current trajectory of the clients has a 73% probability of success. Our minimum acceptable success probability for clients is 80%, which means there is room for improvement.

- The current savings rate of 16.3% is on the lower end for individuals in their age group.

- Cash Flow Analysis:

- A significant portion of their funds seems unaccounted for. These unallocated funds likely result from their previous financial commitments, such as funding their children’s education. It’s common for individuals to spend unaccounted funds because they lack a dedicated plan for those resources.

To address this issue and ensure a more secure retirement, we recommend the following strategies:

Initial Recommendations:

- Continue Maximizing 401(k) Contributions: Since the clients are in the highest earning bracket, they should continue maximizing their contributions to 401(k) accounts.

- Leverage Back Door Roth Contributions: Linda is eligible for a backdoor Roth IRA contribution every year, which can provide additional funds for retirement. This strategy can potentially contribute an additional $7,500 per year to Roth IRAs.

- Establish Automated Savings: We recommend setting up an automated monthly deposit of $5,000 into a taxable investment account. This allows the clients to build a $60,000 cushion, which can be used to reassess their expenses now that their children’s educational costs are no longer a factor.

- Review Investment Allocation: It’s essential to reevaluate their current investment allocation to ensure they are taking on an appropriate level of risk.

With these recommendations integrated into their financial plan, we assess the resulting changes:

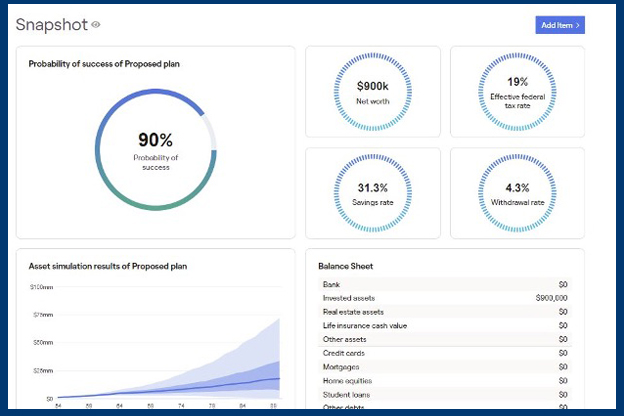

The clients’ probability of success has significantly improved from 73% to 90%, demonstrating a much more secure financial future. Their savings rate has also increased to 31.3%, which aligns with the higher end of the scale for individuals in their age group. With these initial recommendations and continued planning and adjustments, the clients are well on their way to achieving their dream retirement. If you are approaching retirement and would like an assessment similar to this one, please click the link below to schedule a consultation.