Global economic uncertainty continues to drive markets as we enter the 4th quarter. The S&P 500 Index increased by 1.19% for the 3rd quarter coupled with an increase in volatility and trade headwinds. The volatility trend has continued into October however U.S. equities were negative for consecutive days to start the quarter. This has been attributed to ISM data revealing contractions in both the manufacturing and services sectors.

Global trade uncertainty is the main source of a slowdown within the U.S. and world economies. There remains no resolution in sight in the U.S.-China trade war. The U.S. imposed new tariffs on the E.U. on October 2nd and Japan and South Korea continue to be in a stalemate with trade. Economies around the world are beginning to show cracks in their foundations but the U.S. is the most insulated.

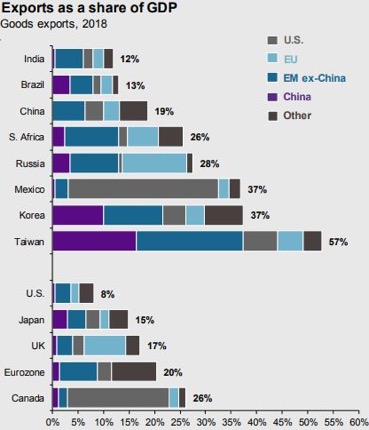

As seen in the chart above from JPMorgan, U.S. exports account for a much smaller percentage of GDP than most other global economies. Over the long-term, revised trade agreements should be beneficial for the U.S. yet it is the biggest risk to global markets in the near term.

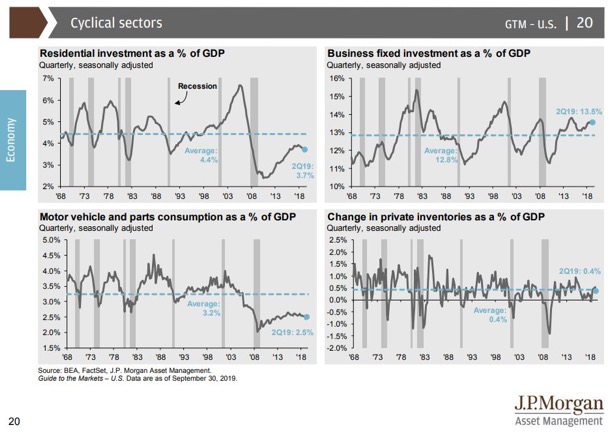

Another word appearing in headlines more is recession. Several economic indicators are flashing warning signs of recession. Trade uncertainty remains the most likely cause behind this weak data. Business’ fixed investment costs are the main drag as CEOs wait for clarity on trade policy. The economy appears resilient with no sign of a bubble in the four major cyclical sectors of the U.S. economy as seen in the charts below from JPMorgan.

Interest rates remain low and economists are expecting further rate cuts from the U.S. Federal Reserve in 2019. This should help curtail weakness in the economy as inflation also remains low. If there is any resolution in global trade policy, it will only provide a tailwind to U.S. and global markets.

The recession has been a hot topic among many financial pundits and we wrote about this recently on our blog. Market psychology and sentiment continue to be drivers of recession fears. A lot of this discussion is a result of the U.S. economy going on its 123rd month of expansion, the longest on record. There are small tremors appearing within the global economy, but it is not clear if they are signs of impending doom or will add up to any larger shock.

The economy appears to be slowing down but there are no signs of an outright stall or recession at this moment. U.S. GDP continues to grow modestly with estimates around 2% for 2019. Despite the negative sentiment, unemployment remains low, home construction continues to rise, and the S&P 500 is up 15.19% year-to-date, within 5% of the all-time high. Trade policy will continue to be a headwind to growth in the economy and equity markets. Any trade agreements or clarity around policy should improve sentiment and could provide a stimulus to growth.