Case Study: Helping High Earners Plan Cashflow

*To ensure confidentiality, all names in this document are fictitious to the best of our knowledge.

A few months ago, a couple approached Blue Bell Private Wealth Management seeking assistance in establishing a financial plan. Now in their mid-30s, they had not previously sought financial guidance and had managed their finances on their own. This was their first foray into working with professional financial advisors. They realized the importance of having a comprehensive financial plan and sought our expertise to help them achieve their goals.

Client Profile

Age: mid 30’s

Combined Annual Income: $232,000.00

Expenses: $107,915.00

Net Worth: $316,870.00

Overview

- To maximize tax efficiency and annual savings, leading to an improved cash flow and probability of success.

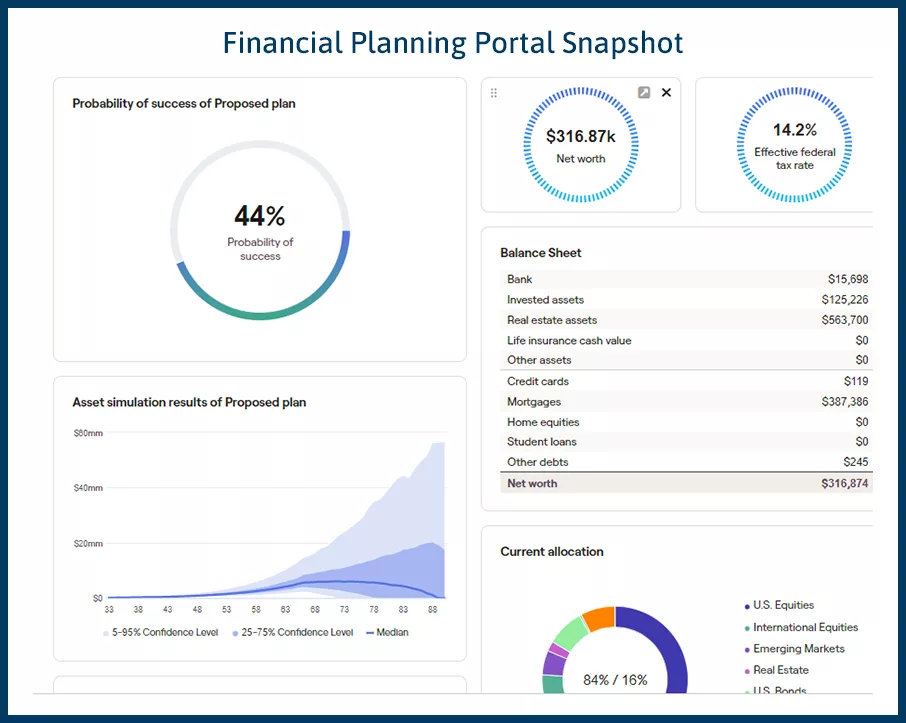

As a part of our onboarding process, we gathered all relevant information and input it into our financial planning portal. Here is an overview of John and Linda’s current financial situation:

Overview and Assessment

It is not unusual to come across young high earners who keep most of their assets in pre-tax 401(k)s due to automatic savings. In this case, it is 6% per paycheck with a 3% employer match. While this is a positive start, we believe there are opportunities to automate savings across all types of accounts and better diversify one’s tax situation.

To achieve this, we gather information on their income, expenses, and planned savings. We then take a comprehensive look at their cash flow to identify potential areas for optimization. Here is a snapshot of what we analyzed:

Analysis

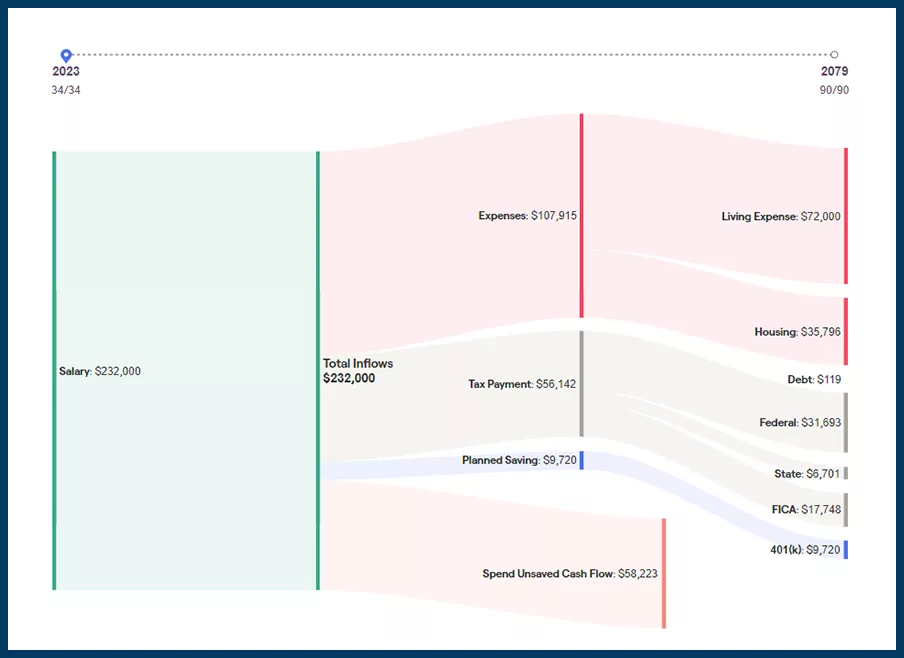

In this scenario, their combined income is approximately $232,000.00, their expenses are $107,915.00, taxes are approximately $56,142.00, and they expect to save $9,720.00. Upon review, we noticed their savings rate is around 7.2%, below the minimum recommendation of 15%. Additionally, there is an opportunity to invest nearly $60,000.00 of their cash flow, which could significantly improve their long-term financial standing.

Recommendations

- Increase savings

- Establish and optimize a Backdoor Roth IRA for each individual

- Establish a taxable joint account

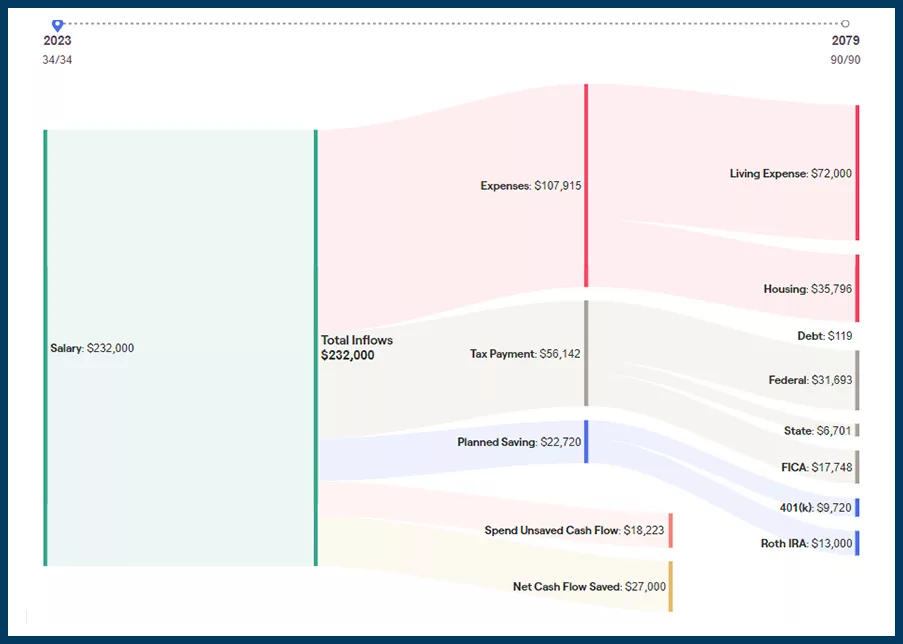

To start, we often find that people underestimate their expenses, so instead of planning to save the entire 60K, we typically start with a more conservative estimate of around 40K. One of our early recommendations was for John and Linda to complete backdoor Roth conversions annually. They each make too much income for regular Roth IRA contributions and have no traditional IRA money, this strategy allows them to each get $6,500.00 into Roth IRAs every year.

We also suggested automatically saving the remaining $27,000.00 ($40,000 – $6,500 – $6,500) in a taxable joint account to diversify their tax situation. To achieve this, we helped them set up automatic savings of $2,250 each month, which ensures that the money is saved and not spent unnecessarily.

Outcomes

After implementing these strategies, their cashflow situation improved significantly, as shown below:

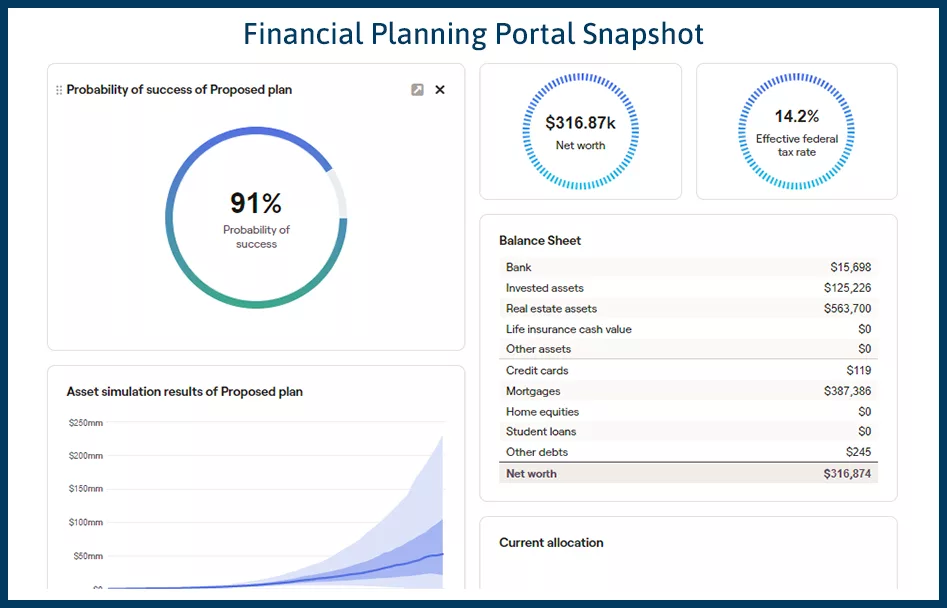

As a result, they were able to increase their savings rate to 24.4% and provide an excellent combination of savings options. It’s also important to note that these recommendations will help John and Linda achieve their long-term financial goals and build wealth for their future. Additionally, a buffer of $20K provides a financial cushion for unexpected expenses or emergencies.

Their probability of success increased by almost 50%, from 44% to 91%:

At our firm, we believe that each person’s financial situation is unique. We don’t offer one-size-fits-all solutions. We take the time to get to know our clients’ goals, expectations, and financial circumstances before developing personalized planning recommendations. This ensures that our clients receive tailored advice that is specific to their individual needs and objectives.