Blue Bell Private Wealth Management

Understanding Market Volatility Through a New Working Hypothesis – “The Inelastic Markets Hypothesis”

By: Mike Weber, CFP®

Key Takeaways:

- Understanding of research terms is important to implementation in real life.

- Know how to interpret what you hear/read and what questions to being asking.

- Better understand recent increases in market volatility and impacts on your personal financial planning/investing by review of “The Inelastic Markets Hypothesis”.

Need to speak with an advisor, click here to schedule a 20-Minute Consultation on Mike’s calendar now.

Intro:

After the severe impact of the 2008 Financial Crisis began to resolve over the follow decade, I began to anecdotally feel that something felt different about the market’s overall behavior. At times, it seemed like new information coming out would lead every individual company’s stock to go up or down together in lock step.

My understanding at the time based on the prevailing scientific theories based on empirical evidence was that this didn’t make logical sense. These theories overwhelming stated that the market is efficient, elastic, and if not, arbitragers would instantly step in to take advantage bringing the markets back into equilibrium.

I begin to hypothesize over the years that the rise of Exchange Traded Funds (ETFs) and the prevalence of index investing was the likely reason for what I believed to be inefficiencies in the market (i.e., everything reacting the same way to new information being introduced to the market).

I’m not an academic or scientific researcher, so I kept to well-known fundamentals of investing like diversification, asset allocation, correlations, financial statistics, and calculations, etc. I never began a rigorous experimentation of data, eliminating data bias, creating a framework to theoretically and empirically analyze my hypothesis to test if there was a broader scientific theory to be proven.

Ok…I think that is enough jargon and scientific terms to get our minds thinking and maybe make you believe I have some higher level of intelligence than reality suggests. Luckily for us all, the world is full of people with brilliant minds doing this type of real research every day and continuing to expand our understanding of space, society, finance, health, medical treatments, etc. For the rest of us, I’ll simply propose we must have the curiosity to learn, ask questions and seek truth through facts.

This article will define a few of the above terms so we can all understand what we read/hear in media and begin to think about the questions we should ask.

Then we’ll explore a new “working” hypothesis, “The Inelastic Markets Hypothesis” written by Xavier Gabaix, Harvard University Department of Economics and Ralph S. J. Koijen, University of Chicago Booth School of Business published in the National Bureau of Economic Research in June 2021 and how this hypothesis could or could not affect your future financial planning and investment strategies.

Terms:

Data – facts collected with real life information or statistics.

Bias – tendency, inclination, or prejudice toward something or someone.

Data bias – dataset does not accurately represent a model’s use case, resulting in skewed outcomes, low accuracy levels and analytical errors.

Evidence – available body of facts or information indicating whether a belief or proposition is true or valid.

Empirical Evidence – information acquired by observation or experimentation.

Anecdotal Evidence – story evidence, often can’t be proven or disproven.

Logical Evidence – information inferred by deductive reasoning.

Hypothesis – proposed explanation made on basis of limited evidence as a starting point for further investigation.

Theory – multiple definitions and uses. “Scientific Theory” is an understanding based on already tested data and results. “Theory” is also used colloquially as a proposed explanation that is subject to experimentation, i.e., an educated guess, “I have this theory…”. Used this way, it is more accurately defined as a hypothesis.

Why is it important for us all to understand these terms you ask? Good question. In today’s society and in various sources of media coverage, we are constantly hearing these terms and they are often used inaccurately to make us believe something is a fact or that someone’s belief is unequivocally true. We’ve all heard of media or political “spin”, so just add the words “fact”, “evidence” or “theory” and it must be true.

Let’s explore a few examples of empirical evidence, anecdotal evidence, and logical evidence that we all have likely heard of:

- Einstein’s Theory of Relativity is a “Scientific Theory” based on empirical evidence and went on to transform theoretical physics and astronomy.

“Einstein stated that the theory of relativity belongs to a class of “principle-theories”. As such, it employs an analytic method, which means that the elements of this theory are not based on hypothesis but on empirical discovery. By observing natural processes, we understand their general characteristics, devise mathematical models to describe what we observed, and by analytical means we deduce the necessary conditions that have to be satisfied. Measurement of separate events must satisfy these conditions and match the theory’s conclusions.” *Einstein, Albert (November 28, 1919). “Time, Space, and Gravitation”. The Times.

- Critical Theory, Critical Legal Theory, and Critical Race Theory (CRT) are hypotheses based on anecdotal evidence and currently having a major impact in politics and society today.

- A juror linking evidence provided by the prosecution is based on logical If the juror believes the prosecutor has not linked the crime to the defendant without a shadow of a doubt, then they have a moral and societal obligation to conclude that the defendant is innocent in our legal system. If DNA, fingerprints, video, witnesses, whereabouts, timeframes and/or other evidence can be logically linked to the defendant as the perpetrator of the crime then the juror must find the defendant guilty.

Based on these three examples we can begin to understand the distinct difference and reliability of the terms being used. Empirical evidence is repeatable and undeniably true. Anecdotal evidence may or may not be true but could lead to research, tests, and studies to gather data for statistically relevant information leading to a truth. Logical evidence can lead us to a conclusion; however, logic varies by our own experiences and can lead to bias.

Today, science and technology allow us to have irrefutable evidence like DNA, fingerprints, and video/audio. This has not always been the case and evidence of bias in logic can be seen with past convictions being overturned with this newly available irrefutable evidence. A reliance of these new forms of evidence today that were not previously available, could mean comparing datasets pre and post these new technologies could lead to data bias.

The next time you see or hear these terms, I hope you’ll ask questions and better understand the users’ intent in the use of the terms. There is a lot more complexity than most of us realize into how a real scientific theory is proven and how simple it can be to use the terminology to create a false sense of facts. I’m certainly not saying we all must be analytical by nature or scientists, but we can all respect the science behind deriving facts that others can use in their decision making.

The following authors make it very clear to the reader that this is a hypothesis, and their intent is to create a platform for further research and development using their framework.

Review of “IN SEARCH OF THE ORIGINS OF FINANCIAL FLUCTUATIONS: THE INELASTIC MARKETS HYPOTHESIS” By Xavier Gabiax and Ralph S.J. Koijen

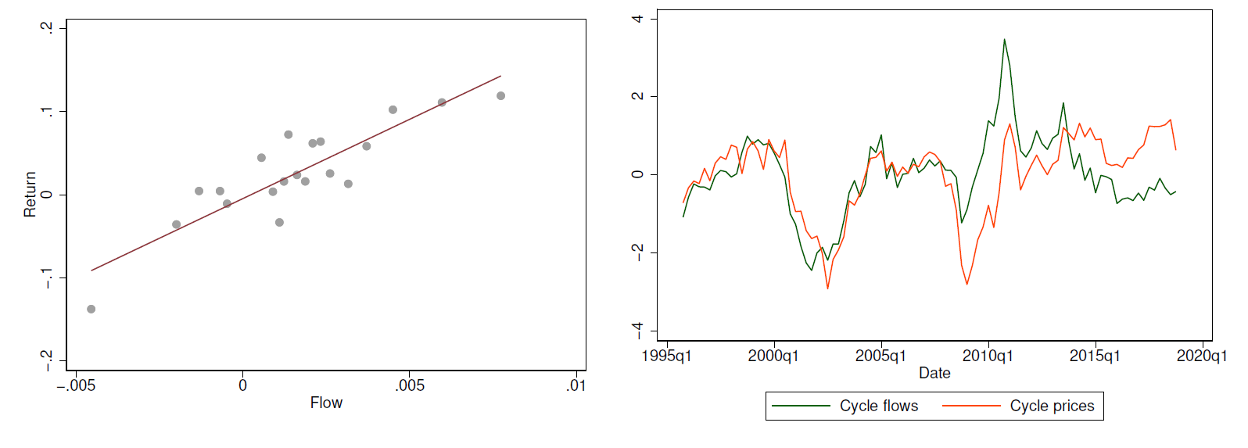

The paper begins with Gabiax and Koijen asking a question: what happens to the valuation of the aggregate stock market when an investor sells $1 worth of bonds and buys $1 worth of stocks?

Using existing theoretical and quantifiable empirical evidence along with mathematics they find that if investors create a flow of 1% of the value of equities that the value to the aggregate equity market goes up 5%.

They also find that a permanent shift in the demand for stocks must create a permanent shift in their equilibrium price (higher demand, higher prices).

Existing and widely accepted theories start with “micro” factors and then extend them to the broader market. For example, looking at Ford and General Motors as close substitutes for investors, such that if Ford has a production problem or low product demand an investor could simply sell Ford and buy General Motors, i.e., high elasticity.

Gabiax and Koijen (along with some other more recent researchers) reason that “macro” elasticity is very low suggesting that stocks and bonds are not considered close substitutes by investors. Therefore, when there is a demand shock to stocks or bonds there is only a slight change in demand for either stocks or bonds.

This research has a significant impact in several real-life financial problems for further debate, like during an economic crisis should a government buy stocks as a policy tool (Japan started doing this in 1998, a decade later US (TARP) and European countries did the same) or the decision of a firm to increase dividend payments or buy back company stock. There are many questions that bring in various societal issues and one size fits all may not be an appropriate application of anything in real life.

Traditional theories of “elastic” markets suggest changes in flows wouldn’t matter much in terms of the impact of market prices, aggregate value to the market and that prices should remain the same ($1 into equities or $1 in dividends wouldn’t matter because there would be no change in the aggregated value of equity markets).

“In contrast, in an inelastic world, the value of equities goes up, by a tentative estimate of around $2.2 As a naive non-economist might think, “if firms buy shares, that drives up the price of shares.” A rational financial economist might say that this is illiterate. But the naive thinking is actually qualitatively correct in inelastic markets. Hence, potentially, as share buybacks account for a large portion of flows (they have been about as large as dividend payments in the recent decade), corporate actions account for a sizable share of equity purchases, and therefore of the volatility and increase in the value of the stock market. This “corporate finance of inelastic markets” is an interesting avenue of research.” (Gabaix, Koijen “The Inelastic Markets Hypothesis” Page 4)

The below graphs show the correlation between flows into/out of stocks and returns.

*(Gabaix, Koijen “The Inelastic Markets Hypothesis” Page 31)

A very generalized conclusion is that in “inelastic markets” flows have a significant impact on the price of the aggregate stock market. This may seem rational to most but has largely been explained away by previous research with the concept of “arbitrage”.

Arbitrage is effectively taking advantage of inefficiency in prices within a market. For example, if the price of a stock is too low, the “smart” money will step in to buy the stock until it reaches fair value and therefore the market is always efficiently pricing the entire value of the stock market. Alternatively, if the price of a stock is too high, the smart money will step in to sell the stock until its fair value is achieved.

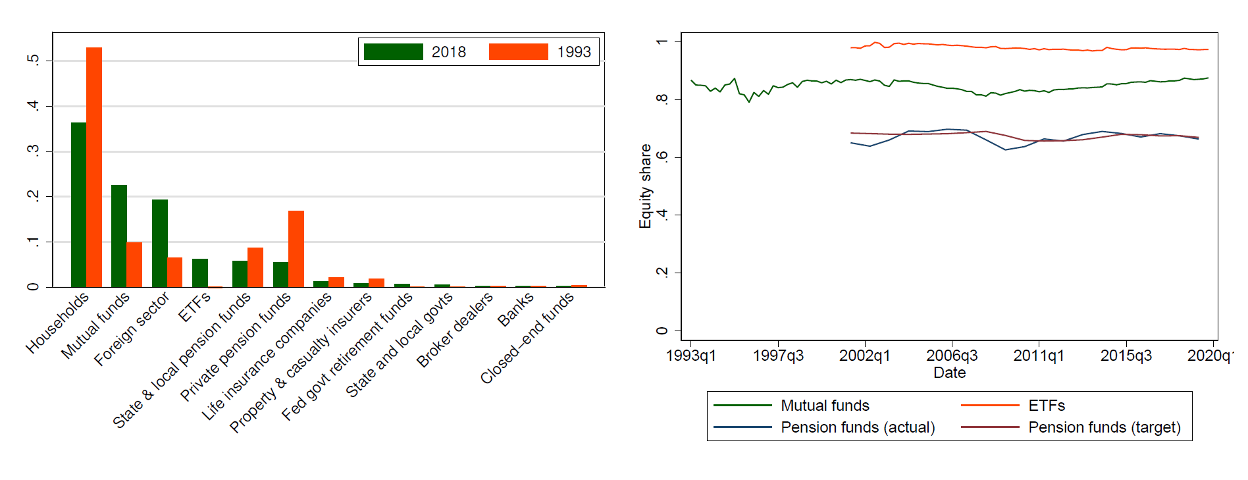

Many of us may think this “smart money” is coming from hedge funds, broker dealers or large institutions, however hedge funds are quite small holding below 4% of the equity market, broker dealers hold a smaller amount less than 0.5% and institutions have stable equity share rarely changing the amount of equities they own.

During the financial crisis research shows that hedge funds sold a relatively small amount of the entire equity market equal to 0.1% of the market per quarter from 2007.Q3 to 2009.Q1. In addition, mutual funds and other institutions have tight mandates in terms of what percentage of equities they are required to hold.

Equity Share by Institutional Sector & Change In Equity Share Graphs

* (Gabiax, Koijen “The Inelastic Markets Hypothesis” Page 8)

Therefore, who would be doing this arbitraging? The article views this smart money arbitrage assumption of “elastic” markets as unlikely and further evidence that financial markets are “inelastic”.

Gabiax and Koijen’s paper find, “both theoretically and empirically, that the aggregate stock market is surprisingly price-inelastic, so that flows in and out of the market have a significant impact on prices and risk premia.” (Gabiax, Koijen “The Inelastic Markets Hypothesis” Page 41)

I do not think it would be appropriate to go through the entire 52-page research paper lovingly filled with mathematical equations and proofs that nearly made my head exploded, however I do believe that this continued research will prove very interesting. In addition, I believe it changes the way clients need to think about volatility, income, cash flow, and long-term investing or may in-fact prove the way some already do think.

Impact on financial planning decisions and investment management

I may sound like a broken record, but again I think this paper highlights the importance of financial planning for individuals and families. At its face value, this paper may appear to have little to do with financial planning for households. I would disagree. It has much to do with household financial success.

I have always believed that individuals and families get the most success from prudent investment management and financial planning. If you’ve ever worked with me, you’ve heard me talk about things like only investing money for longer term goals (i.e., if you need the money in a year or two for a goal like your kids’ education, it should be in safe zero risk of loss investments like savings accounts, CDs, or a little more risky short term investment grade bonds or municipal bonds depending on risk tolerance and the interest rate environment), having adequate cash resources for an emergency to maintain the power to decide when to buy or sell an investment, understanding current and future cash flow needs to determine the amount of investment risk required to achieve your goals, planning for estate planning needs in the future, etc.

These are all financial planning conversations, honestly, I could go on and on. The point is understanding markets leads to smart financial planning decision making.

There are some things we just must accept. One is that if you want to make stock market like returns, your risk tolerance must reflect that, and you must plan for volatility. Another is that given the size of our markets, many things are outside of our control, like interest rates and government fiscal policy.

If you thought hedge funds and institutions were large enough to arbitrage our markets into a beautiful state of efficiency and equilibrium, I think we need to guess again. It is possible that the “invisible hand” of Adam Smith is in fact doing this, but the bigger question this article is exploring is how shocks to the system, also known as market or systemic risk (the risk we can’t diversify away from), effect market prices based on flows into and out of the equity markets.

From an investment management standpoint, this means our understanding of existing investment theories needs to change and, like our firm’s investment management strategies, we need to be creative when addressing portfolio asset allocation and portfolio “risks”.

After the 2008 Financial Crisis, many market strategists said that the 60/40 ideal portfolio was dead and there would be a “new normal” of a lower interest rate environment, geopolitical risks, along with inflation pressures. In 2020, they may have been proven right. With interest rates on investment grade fixed income again yielding negative “real” interest rates (rates lower than inflation expectations), the next several years again presents real concerns with owning bonds.

We must remember that only high-quality bonds like U.S. Treasuries, high quality municipal bonds and investment grade corporate bonds have a diversification benefit to a portfolio to reduce risk as defined by volatility. When stretching for yield into “junk bonds” or low-quality fixed income there is little diversification benefit as these bonds have historically had an above 90% correlation to stocks.

In my mind, this means the Vanguard “strategic” portfolio strategy is also dead. Vanguard is an amazing company and pioneer for the regular investor; however, I fail to see how such rigid strategies will prevail into the future. Simply put, owning the entire stock market with a certain percentage of the entire bond market based on age would seem to defy the realities that global economies have been dealing with since 2007. I will say, however, that I will continue to buy their ETFs though, if they are cheaper than the increasing number of competitors offering the same exact indexes and newer more innovative low-cost ETFs. Diversified index investing is being commoditized down to a no value proposition for any mutual fund company.

I think we can argue that during certain market conditions the idea of safe income investments like bonds cannot provide the income and protection that retirees look for in investments. During these times, we need to focus on “cash flow” and not necessary the consistent income bonds can provide.

We need to be flexible, smart, and adjust our strategies according to market and economic conditions, also known as “tactical” asset allocation. I have believed this for a long time, increasing my beliefs every major market crisis.

In conclusion, the working research paper on “The Inelastic Markets Hypothesis” further helps me understand what I have seen and felt in the markets since 2007 when you could buy U.S. Treasuries yielding over 5% at zero risk and inflation below 3% but people were buying REITS with under 1% yields and other risk assets instead. All along, I heard and read markets are efficient, all knowing, rational, etc. I think, it’s people’s greed that drives flows irrationally into investments until the system literally breaks.

It helps me begin to explain why at times, investments that have low correlations to each other historically move up or down in lock step at certain times of systemic volatility. I’m excited for further research in “The Inelastic Markets Hypothesis” and if you’d like to read the working paper you can go to http://www.nber.org/papers/w28967.

You can schedule a 20 Minute Consultation on my calendar here.

Let me know how I can help you. Contact me at:

Mike Weber, CFP®

Investment Advisor Representative

Blue Bell Private Wealth Management, LLC

484-221-5408