Executive Summary

So far this year there has been a lot to be positive about from an economic perspective. Record amounts of monetary and fiscal stimulus has led to record consumer savings and wealth. Pent-up demand and higher wages are propelling consumer spending, leading to record earnings and profit growth for many companies. To date, 86% of S&P 500 companies have reported a positive EPS surprise while 83% have reported a positive revenue surprise. This marks the highest year-over-year earnings growth rate reported by the index since the fourth quarter of 2009.

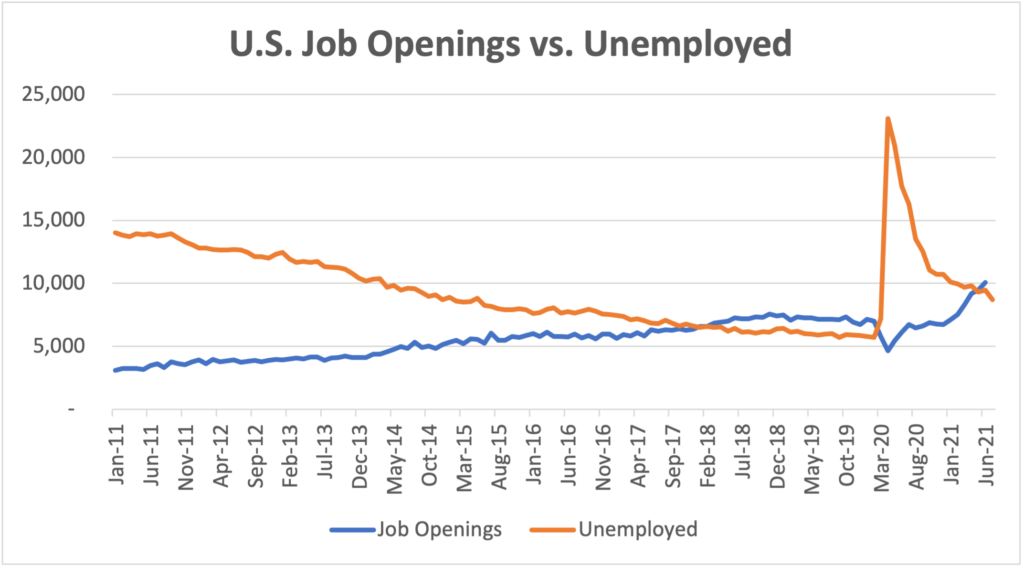

The unemployment rate has fallen to 5.4% as more people head back to work. Notable job gains have been driven in large part by the leisure and hospitality sectors as the economy continues to recover from closures due to COVID and vaccination rates increase. Wages rose 4% on an annually adjusted basis suggesting that increasing demand for labor has put upward pressure on wages. Interestingly, job openings have reached record levels and now eclipse the number of people who are unemployed by approximately 1.3 million. Quit rates also remain at historic highs hovering around 2.7% suggesting that job seekers are in a strong bargaining position despite elevated unemployment. With unemployment benefits set to expire and schools reopening, labor supply is expected to pick up, which should lead to a gradual improvement in labor market conditions1.

Inflation had trended above the Federal Open Market Committee’s 2% target since March with the most recent core PCE reading rising 3.62% annually. During speeches held at the Jackson Hole summit, Federal Reserve Chairman Jerome Powell reemphasized his belief that the uptick in inflation is due primarily to transitory effects stemming from supply chain disruptions. In addition, the Fed discussed possibly reducing the size of their asset purchases by the end of this year. As of now, the FOMC buys $80 billion worth of Treasuries and $40 billion worth of agency mortgage-backed securities per month which help to support accommodative financial conditions. Powell, however, reiterated that any increase in interest rates will be subject to the higher standard, as laid out in the Committee’s outcome-based guidance on the federal funds rate2. As of now the market is not pricing in the possibility of a rate hike until January 26, 2022, and that probability only stands at 2.0%.

The markets continue to take the economic data in stride. Charles Schwab and their Chief Investment Strategist Liz Ann Sonders has some interesting observations. As of August 31, 2021, the S&P 500 has gone 210 days without at least a 5% drawdown. The maximum drawdown year-to-date has been -4.2%. There have only been three calendar years since 1928 where the maximum drawdown was less than that: 1964 (-3.5%), 1995 (-2.5%), and 2017 (-2.8%). While periods in 1965, the mid 1990’s, and 2017 saw stretches as long as 400 days, the current streak could still be considered statistically significant2.

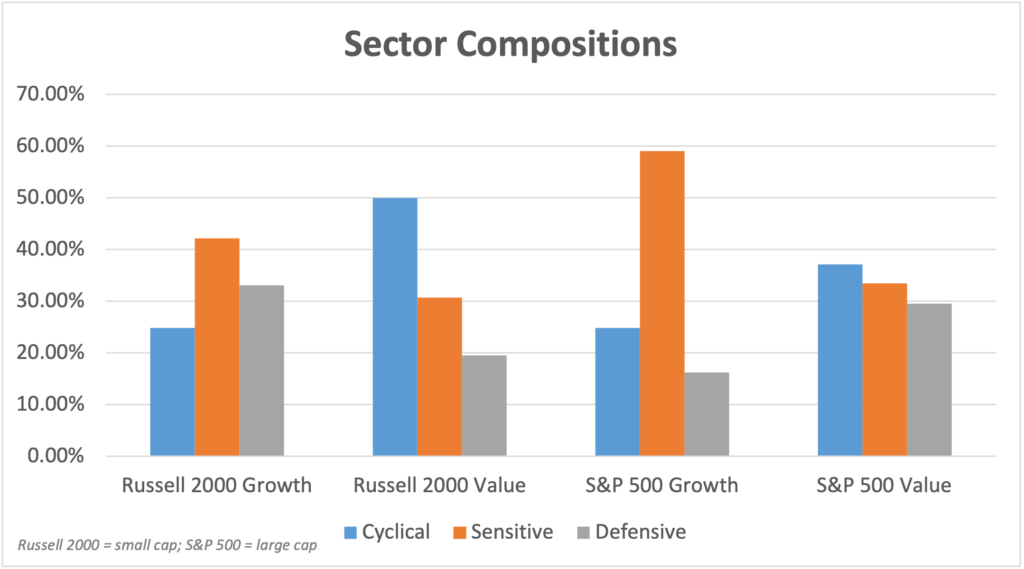

With the increase in underlying earnings, we have seen the forward S&P 500 P/E fall to its current level of 21.43x, although this remains elevated from a historical perspective. For the month, the S&P 500 gains were lead in large part by financials, materials, and technology but throughout the year the various sectors’ returns have illustrated the need to stay diversified. Over the past three months, as fears about interest rate increases have abated, large cap growth stocks are now in line with value stocks, erasing much of the underperformance seen in the first half of the year. This is in stark contrast to small capitalization companies where value has outperformed growth by a wide margin. In previous Monthly Market Updates, we discussed how the sector composition between large and small caps can unveil a lot about their recent performance. Small caps are dominated by financials, industrial, and real estate stocks which are more cyclical in nature and tend to outperform coming out of recessions. The value index further magnifies those differences, adding even more to those sectors, which has contributed to the wide disparity in returns.

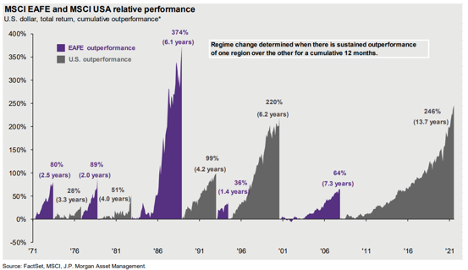

Internationally, valuations and yields remain attractive compared to those in the U.S. Even with recent downward revisions from the International Monetary Fund (IMF), emerging and developing economies are still expected to grow at 6.3% and 5.2% for 2021 and 2022 respectively. This is higher than their advance economy counterparts who have projections of 5.6% and 4.4% respectively over the same time periods4. We remain in a somewhat unprecedented period of U.S. equity outperformance, but the chart below helps to illustrate the benefit of being diversified across geographic regions at different points in time.

Looking forward several risks are still prevalent. Only 53% of the population is fully vaccinated as the Delta variant drives new cases and hospitalizations higher. Consumer sentiment plunged in August to its lowest reading since 2011, surpassing the lows reached in April of last year during the pandemic, on the back of fears that the virus will reduce the momentum of the broader economic expansion5. Missteps in monetary policy, deteriorating market breadth, political unrest, peak earnings, and extended valuations all have good cause to create increased market volatility moving into the last four months of the year. As usual, we recommend taking a diversified approach and avoiding trying to time market highs or lows. Speaking with an advisor you trust and ensuring your portfolio is aligned with your objectives and risk tolerance will only help to see you through periods of turbulence and avoid costly mistakes. If you have any questions about your portfolio or would like a complimentary review, please do not hesitate to reach out.

1 – Goldman Sachs Asset Management – Chart of the Week

2 – Minutes of the Federal Open Market Committee July 27-28, 2021

3 – Charles Schwab – You Take My Breadth Away: Market’s Underlying Deterioration

4 – Fault Lines Widen in the Global Recovery – July 2021

5 – Ned Davis Research – U.S. Daily Economic Perspectives (August 13, 2021)